_36.jpg)

Kuwait Financial Centre “Markaz” recently published the executive summary of an updated version of their GCC infrastructure series covering: Power, Airports, Seaports, Roads & Railways, ICT and Water.

For the past several years, GCC countries have made concerted efforts toward enhancing their power generation capacity in an effort to satiate rising demand due to the increase in the population and economy. Power consumption across the GCC has grown at an annual rate of about 9% from 2002; Saudi Arabia and the UAE account for a combined 75% of the total GCC consumption.

The major power projects, completed across the GCC during the past decade, have now commenced operations; installed capacity has doubled from nearly 46,600 MW in 2002 to almost 98,000 MW in 2009: a CAGR of 10%. The year 2009 saw a massive 23% increase in capacity as several plants in Qatar and Saudi Arabia started operations. Currently, the GCC operates with a reserve margin of about 19% with an excess reserve mainly in Qatar and Abu Dhabi (43% and 30%, respectively).

Furthermore, the GCC power grid has successfully passed through two phases and now entered its third and final phase: the inclusion of Oman. Saudi Arabia, with the largest installed capacity, is expected to be a major player in the selling of power and has begun studying the possibility of linking the grid to North Africa and even Europe.

The GCC states have also begun exploring alternative sources of energy including solar power, nuclear, and natural gas in an effort to boost capacity and diversify the energy mix.

Demand is expected to grow at between 7% and 8% annually over the coming years, and the GCC counties are expected to spend US$45 billion until 2015 in order to add an additional 32,000 MW of capacity.

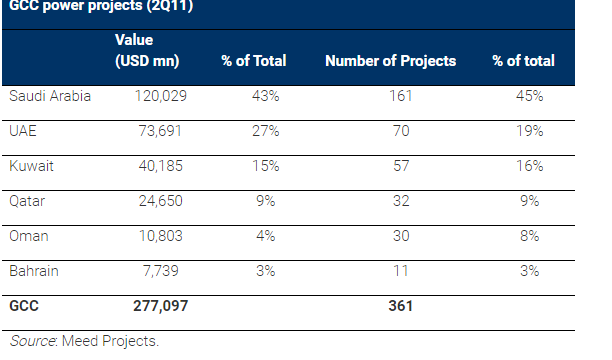

According to Meed Projects, there are currently 361 power projects (generation, transmission, substations, and so on) throughout the GCC with a total value of US$277 billion. The majority of these projects are in Saudi Arabia and the UAE: a combined contribution of 70% of the total. Saudi Arabia has the highest number of projects at 161, followed by the UAE at 70 projects.

The global slowdown has impacted the GCC with 11% of projects “cancelled” (with a value of US$31 billion) while 3% are currently “on hold.” Over half of the cancelled projects (15) are in Saudi Arabia with a value of US$17 billion while US$5.4 billion worth of UAE projects have been cancelled.

One-third of the projects (with a value of US$92 billion) are in the execution phase, and these are mainly based in Saudi Arabia (73).

The GCC is set to increase capacity due to ambitious growth plans following the strong “post-08/09 crisis” oil price to satisfy fast-growing energy needs. The speed and quality of development are varied, and depend on a specific country’s needs and approach. Thus, Kuwait has witnessed the slowest rate of annual growth in power consumption during the last decade at 6% whereas consumption in the UAE and Qatar has grown at around 15%.

Although the power sector has seen major structural changes around the world and especially in developed countries, the microeconomics of power production and especially distribution (selling and pricing) remain antiquated in the GCC. This may be a hindrance toward adopting modern frameworks and financing structure for new projects.

Supply Catching Up with DemandApart from Kuwait, whose reserve between production and consumption is only 10%, other GCC countries have relatively more comfortable margins. However, the high expected growth rates, will rapidly reduce this reserve. Hence, this factor is a major incentive for the GCC to increase their production to maintain a surplus.

Qatar aims to be a source of power exports after the GCC Power Grid is fully functional; with a reserve margin of more than 40%, it is well placed to supply power to its neighbors. The UAE is also keen to play a role, especially Abu Dhabi, the source of most of the excess capacity.

Saudi Arabia, which has the largest installed capacity, is rapidly streamlining and increasing the efficiency of its power sector in order to play a role in power exports, although the growth in demand hinders its ability to do so. If substantial increases in capacity are not made, the reserve margin could fall to 9% by 2014.

Increasing Role of Private Sector

The GCC countries are gradually welcoming private sector participation in power projects. PPPs are a good first cooperative step instead of pure privatization; this model has been used sucessfully in the GCC for a number of years now. It is true that with surplus revenues and pricing not reflecting the real economics and occasional slow administrations, the environment has not been very conducive to attracting private investment.

Private Participation in Infrastructure

Power was one of the first sectors to be opened up by GCC governments for development by the private sector. Oman has significant experience with regard to PPPs in the power sector—the country successfully set up five power projects with 1,800 MW of power capacity and planned four additional Independent Power Producers (IPPs) with a combined additional capacity of nearly 3,500 MW. The remaining GCC governments have adopted the Independent Water and Power Project (IWPP) model to develop their power and water sectors.

The successful implementation in 2009 of the SAR9 billion (USD2.4 billion) Shoaiba IWPP private sector project—the first of the four IWPPs—with a capacity of 1,191 MW was an inspiration for other IWPPs in Saudi Arabia. SABIC, the Saudi Arabian Oil Company (Saudi Aramco), and the Royal Commission for Jubail and Yanbu joined hands with private investors to set up a utility company, Marafeq, to expand water and power supply in the industrial cities of Jubail and Yanbu, currently having a capacity of over 1,000 MW.

In Kuwait, Sulaibiya Wastewater Treatment and Reclamation Plant was the first large infrastructure project to be carried out by the private sector. In Bahrain, the Al Ezzel power plant and Hidd IWPP are owned and operated by international power developers.

Retailing and Pricing Based on More “Real” Economics

With free energy in Qatar and heavily subsidized energy in Kuwait, major reforms are needed in retailing. However, selling energy to consumers at or above production prices and also incorporating the externalities of pollution costs, is politically very difficult in the GCC. However, the UAE and Saudi Arabia have already started to increase their prices. Dubai, which is not oil-rich, increased the price of electricity (and water) to consumers in March 2008 and has instituted a “slab-pricing” structure whereby the price increases with higher consumption, in an attempt to curb consumption. Emiratis are exempt from the new pricing. DEWA estimates that only 20% of consumers will be affected by the new rate. Saudi Arabia plans to introduce competitive pricing in retailing by 2016.

Governments can always choose to pay Independent Power Producers (IPPs) at a rate which will allow them to make a profit and then sell the electricity to its population at a subsidized price. The business model will work, albeit with a major distortion. The prices obtained by producers will be attractive, but consumers will still have little incentive to save energy. Demand for peak power will not abate, thus requiring more wasteful investment in power generation.

The GCC Electricity GridThis US$1.4 billion project is aimed at meeting rapidly increasing power demand and avoiding shortages. As soon as it is completed, it will provide electricity across the GCC. The second phase (out of three) became operational in April 2011. The grid will provide a platform for energy trade and exchange; it will improve the reliability of existing energy systems and lower electricity reserve requirements. The members are now negotiating to sell power to each other and will be penalized if they do not maintain a minimum reserve level to support their neighbors during an emergency. Oman’s joining is delayed and now expected to happen in two years.

# End #

###

About Kuwait Financial Centre “Markaz”

Kuwait Financial Centre S.A.K. 'Markaz', established in 1974 with total assets under management of over KD 906 million as of June 30th, 2011, is the leading and award winning asset management and investment banking institution in the Arabian Gulf Region. Markaz is listed on the Kuwait Stock Exchange (KSE) since 1997 under ticker Markaz.