_36.jpg)

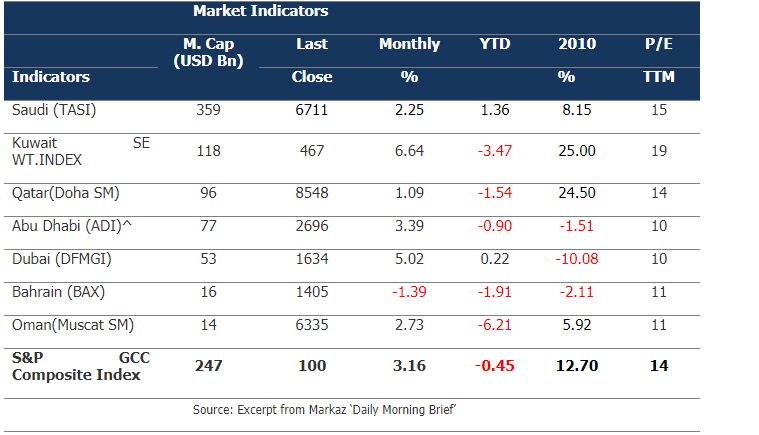

Kuwait May 8th 2011 – The GCC saw additional gains in April, though not a strong as those witnessed in March. The S&P GCC Composite gained 3% versus 6% in March. Returns were lead by a nearly 7% gain in Kuwait’s weighted index and 5% in the DFM. Bahrain was the only market to show continued weakness, losing 1.4% for the month.

Consistent gains in crude oil continue to support local markets; Brent ended at $126/bbl, an 8% monthly return. According to the Institute of International Finance (IIF), the GCC will see a combined current account surplus of over USD 290 bn this year, more than double that of 2010, as oil prices strengthen.

Consistent gains in crude oil continue to support local markets; Brent ended at $126/bbl, an 8% monthly return. According to the Institute of International Finance (IIF), the GCC will see a combined current account surplus of over USD 290 bn this year, more than double that of 2010, as oil prices strengthen.

Q1 earnings came in. Banks did fairly well; ADCB and Emirates NBD had strong showings, with net profit more than doubling for the former and up nearly 30% for the latter. QNB also had strong results; net profit was up 34% on the back of strong lending. NBK net profit was up 6% YoY to almost USD 300 mn while Al Rajhi’s earnings grew just 1% for the quarter.

Industrials also did well on the back of healthy oil prices; SABIC net profit was up 42% in the first quarter to USD 2 bn while Industries Qatar saw a growth of 75%. Telecoms were down; Etisalat saw its Q1 net profit fall 9% while Qtel earnings fell 36%. Zain’s net earnings came in at USD254 mn, a 36% growth. Other big earnings announced included

Aside from earnings announcements, other big news in the region included:

- The possible upgrading of both the UAE and Qatar from Frontier to Emerging Market status in the MSCI universe of indices. The decision is expected in June and analysts, for the most part, are more positive on a Qatar upgrade versus the UAE.

- In Kuwait, it was announced that spending on the Kuwait Development Plan bumped up to KD 1.2 bn in 3Q10 from the KD 735 mn registered in 1H10.

- The Qatar Central Bank cut rates to boost lending, especially towards the private sector where credit demand has been muted. The overnight deposit rate and repo rate were cut to 1% and 5% respectively.

- The UAE telecom regulatory body announced that mobile number portability has been delayed from 2Q to the third quarter of the year.

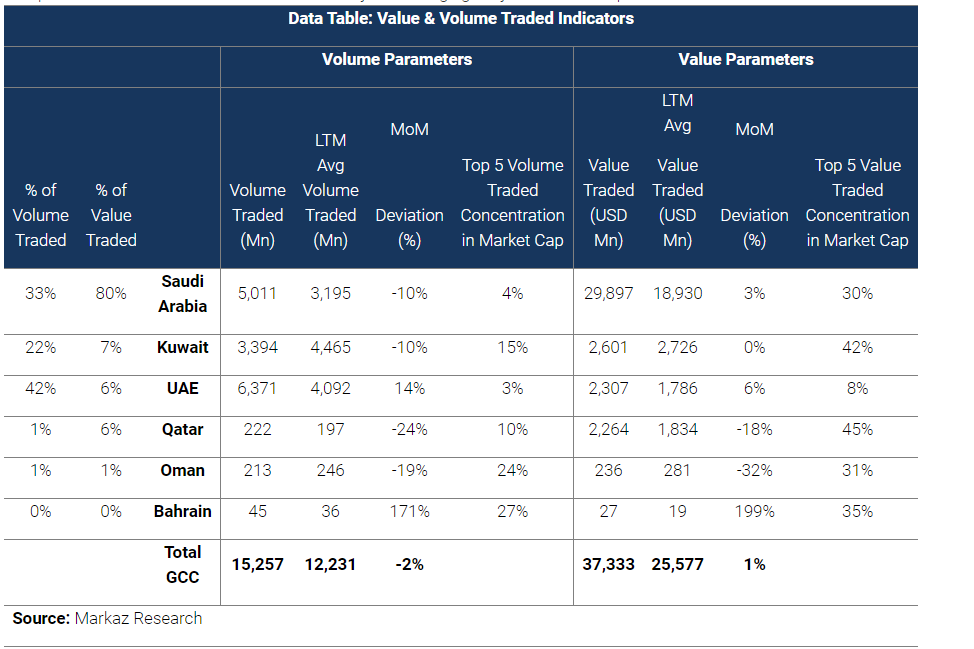

Volume traded declined 2% in April while value was up 1% to USD 37 bn. Saudi Arabia saw a 10% decline in volume while value was up 3% to USD 30 bn. In the UAE, volume and value grew 14% and 6%, respectively, while value traded in Kuwait was flat.

GCC volatility was down by more than half in April, lead by a 60% decline in MVX Saudi while MVX Kuwait shed 41%.

Kuwait valuations have dropped to the 15x-20x range as earnings have grown while Qatar’s valuations have increased slightly closing in on the 15x range.

Global Markets review

World markets were up as European manufacturing strengthened. The US saw a rally despite the S&P credit warning. MSCI World gained over 4% in April, doubling the YTD return to nearly 9%.

The big news during the month was the S&P placing of US debt on watch for a possible credit downgrade from “Stable” to “Negative” which caused the stocks and bonds market to tumble briefly. The warning indicates that there’s a 1 in 3 chance that S&P could lower the rating over the next 6 months to 2 years. On the other side of the pond, European debt is returned to the forefront as Portugal received a USD 116 bn bailout to ease budget strains. The euro has been steadily gaining against the greenback through the year (up 11%), approaching an 18-month high, as European manufacturing strengthened while the USD continues to weaken in light of QE3 and loose monetary policies.

Gold pushed past the $1500/oz barrier towards the end of the month as commodities kept on their upward trend. Crude oil was up another 8% for the month, bringing the YTD return to 36%.

# End #

About Kuwait Financial Centre “Markaz”

Kuwait Financial Centre 'Markaz', with total assets under management of over KD 960 million as of March 31st, 2010, was established in 1974 has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997.