_36.jpg)

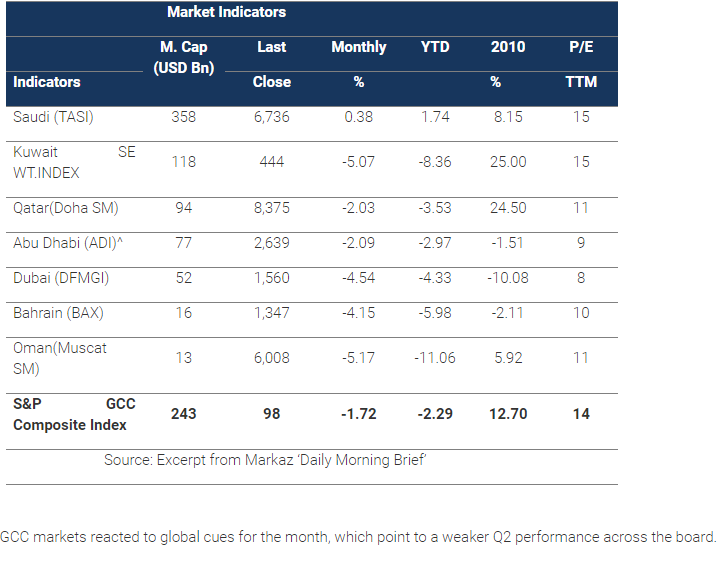

GCC markets reversed April gains, as a wave of selling swept markets in addition to weak global cues. The S&P GCC Index was down 1.72% with Saudi Arabia being the only market to show a gain, closing up just 0.40%, while all other markets lost between 2%-5%. Losses were led by Oman and Kuwait; the former was down almost 5.2% while the latter (Weighted Index) shed 5%.

News in the region included:

- Moody’s cut Bahrain’s sovereign credit rating to Baa1 (from A3) with a Negative outlook due to continued political unrest. According to the rating agency, these events are likely to have damaged economic growth significantly, especially in service sectors such as tourism, trade and financial services.

- The Saudi Arabian Monetary Authority (SAMA) reiterated its commitment to Dollar peg, stressing that it was here “to stay”, despite rumors that all GCC countries (Ex. Kuwait) might de-peg from the greenback within 3 years.

- Dubai, which has a significant debt overhang in the coming years (to the tune of $30bn in two years), is planning to cut government spending by 20%-25% until 2013 in an effort to save almost USD 1 bn and narrow its deficit.

- Fitch and S&P both assigned a ‘AA’ credit rating with a Stable outlook to Abu Dhabi in spite of regional political unrest. The oil-rich emirate accounts for roughly 60% of UAE GDP.

- Qatar is moving ahead with efforts at creating a formalized debt market; the State will first introduce sovereign bonds and Sukuks as part of its plans to soon introduce bond trading, to be followed by Corporate bonds.

- Batelco and Kingdom Holding denied claims that their USD 950 mn bid for Zain Saudi Arabia had hit roadblocks and insisted that all parties were committed to the deal.

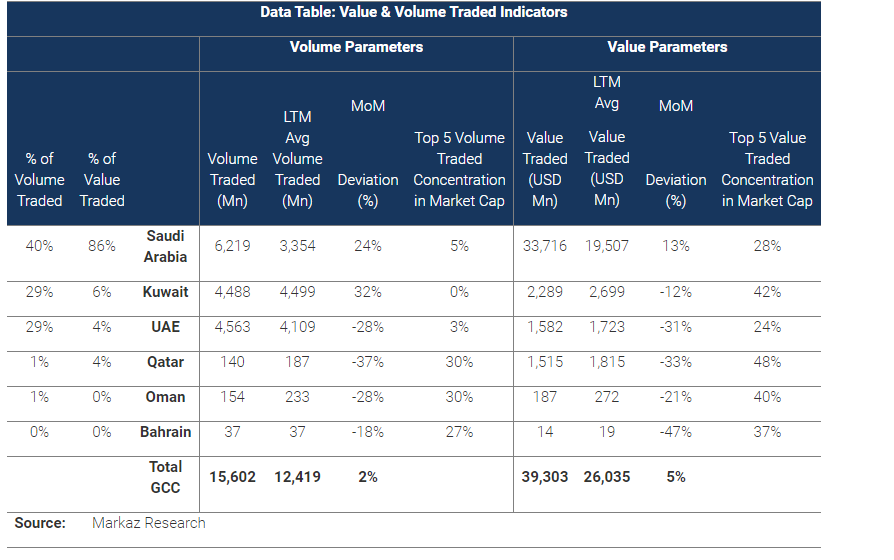

Volume traded was up 2% in May while value traded was up 5% to USD 39 bn. Liquidity was driven by increasing volume in Saudi and Kuwait, where volume traded was up 24% and 32%, respectively, while volume across all other markets were down MoM.

MVX GCC was down 17% for the month, the highest decline in the region was a nearly 40% decline in MVX Saudi. Oman was the only GCC country to see an increase in risk; MVX Oman was up 18% for the month.

Kuwait valuations remain in the 15x-20x range and are trending lower as earnings have grown while Oman is trading at about 10x and Qatar’s valuations have increased slightly closing in on the 15x range.

Global Markets review

World markets fell in the first half of the month before leveling off towards the end as economic data indicated that Q2 would be weaker in terms of global growth. The MSCI World index shed 2% in May, bringing the YTD return down to 6.6%.

The US economy grew by 1.8% in 1Q (missing estimates) while the Euro area grew at just 1% despite strong growth out of Germany. Greece debt issues returned to the forefront as the country struggles to fulfill the requirements of the 5th tranche of its bailout agreement through further austerity measures.

Commodities also seem to be cooling off; the CRB Commodities Index shed 1% for the month after coming in flat in April. Crude oil reversed its April gain with a loss of 7% for the month, but remains up 26% YTD.

# End #

About Markaz

Kuwait Financial Centre 'Markaz', with total assets under management of over KD960 million as of March 31, 2011, was established in 1974 has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997.