_36.jpg)

After severely underperforming Emerging Market peers in 2009, GCC markets performed more on par with the same in 2010; the S&P GCC index has gained 11% YTD versus about 13% for MSCI EM (MSCI BRIC remains an underperformer with a gain of just 3%). A recent report released by Kuwait Financial Centre “Markaz”, “What to expect in 2011”, points out that there was no perceptible difference in the scale and magnitude of issues that haunted the market post financial crisis. Companies are still busy repairing their balance sheets and image, while governments are busy spending with nothing specific to write home about regarding regulatory reforms.

The report notes that while oil prices did not spring any negative surprise in 2010, it was not enough to propel the market. In the wake of mounting pressures in the form of weak earnings, ultra weak liquidity and ever present volatility, stable oil price alone is not sufficient to lift the markets to heights that investors are used to in the past.

One possible reason for the ultra poor liquidity is that retail investors (constituting the backbone) are still busy putting their house in order while sources of traditional funding for stock market (bank lending) has come to a complete halt. Earnings destruction in certain cyclical sectors like the investment sector has been too severe to stage a meaningful comeback. Even the elephant among the sectors i.e., banking, continued to surprise investors with high levels of provisioning. Given firmer oil prices and a better global economic environment, the GCC is set to show stronger growth going forward despite slower private investment/credit growth continuing to be a drag on economic growth. Private demand is expected to remain weak in the intermediate term until investor confidence returns more fully and bank balance sheets return to a healthier state.

Overall, the authors remain optimistic in the New Year with positive outlooks for Kuwait, Abu Dhabi, Qatar and Oman while neutral for others. There are several interesting investment themes at play. We reiterate our strong belief that high volatility should be a source of portfolio strategy rather than a problem. We also provide some ideas in the space of defensives and cyclicals. We believe that GCC is a good yield play. Watching analysts’ coverage can provide some important clues to stock picking. Strategies that benefit in a low liquidity environment are also emphasized. Finally, it is time to remove the wheat from the chaff through the lenses of corporate governance.

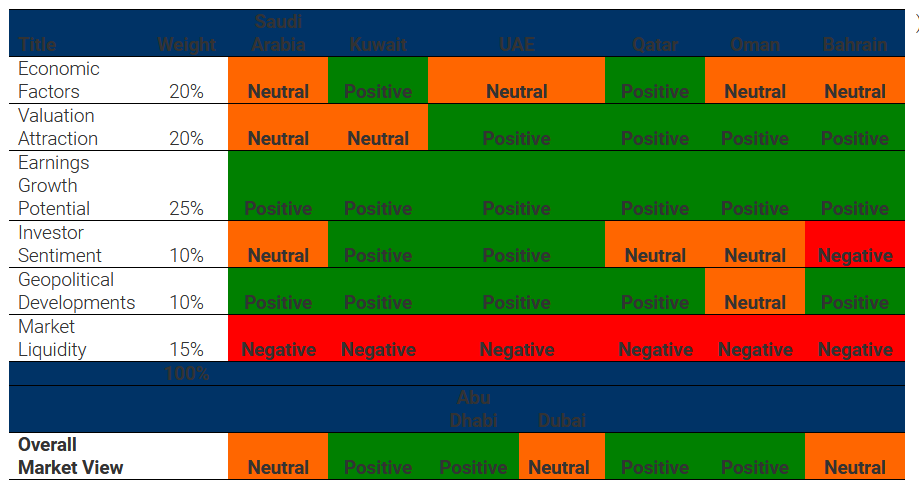

Country Views

Saudi Arabia – Neutral

The report has a Neutral outlook on Saudi Arabia for 2011 due to moderate economic activity and expensive valuation (inflation is a factor to be watched in addition to the struggling real estae sector). Positive factors arise in the corporate earnings segment in addition to the geopolitical and regulatory arenas.

Following the global financial crisis, real GDP growth in the Kingdom was forecasted to push past 4% in 2010; however, continued uncertainty in the region led to the growth rate falling a bit short. Real GDP is estimated to have grown between 3.4% - 3.7% in 2010, a significant improvement from the 0.6% logged in 2009. Healthy crude oil prices are expected to offer some support to fiscal and current balances, despite increased government spending aimed at enhancing growth in the coming years; real GDP growth is expected to be between 4%-4.5% in 2011.

Market liquidity remains a concern for all GCC markets; in the Kingdom, value traded is down by 54% in 2010 (up to November). However, the market remains fairly open to foreign investors and the regulatory structure is relatively sound with active capital market/monetary regulatory bodies.

Kuwait – Positive

The authors are Positive on Kuwait in 2011 due to positive economic indicators and corporate earnings health. One area of concern is in valuations as the market is trading at a PE (TTM) of 20x which seems excessive in our view. Market liquidity, or lack thereof, is also a concern.

Kuwait’s economy is slated to have grown at about 3% in 2010, which would be half the historical average; this growth is expected to bump up to 4.5% in 2011 on high commodity prices, which will maintain the fiscal balance at about 21.5% of GDP. Additionally, the country has enacted a $107 bn, 5 year economic development meant to stimulate various economic sectors. On the corporate earnings side, after the turnaround story of 2010, corporate earnings are expected to resume a more stable course, growing at about 32%. Value traded is down 55% so far in 2010, a further contraction from the 44% decline seen in 2009.

UAE – Abu Dhabi: Positive, Dubai: Neutral

The authors have segregated their UAE outlook and are Positive on Abu Dhabi while being Neutral on Dubai. The economy fell short of its 3% real GDP growth for 2010 and managed an estimated growth of about 2.4%, which is expected to increase to 3.2% in 2011. Inflation was at 2% in 2010 and is expected to bump up to between 2.5% - 2.8% in 2011 as economic growth picks up. Additionally, the geopolitical and regulatory arenas are considered to be stable. However, lack of liquidity remains a problem as value traded in the UAE continues to dry up.

The debt issues in the UAE will continue to be a drag on economic growth as banks provision against possible losses and remain wary of funding new projects. Dubai has over $42 bn in debt obligations due in 2011/2012 and an additional $55 bn beyond that, the service of which will be monitored very closely for signs of possible duress. As the more economically robust emirate, Abu Dhabi will also be watched closely in terms of its support of Dubai.

On the other hand, corporate earnings should return to growth in 2011; after declining by an estimated 6% in 2010, growth is expected at 24% in 2011.

Qatar – Positive

The authors have a Positive outlook on Qatar owing to its high economic growth prospects, healthy banking sector and heavy government support. Qatar’s GDP is expected to have grown 16% in 2010; 2011 growth is expected to be between 15%-18%. High fiscal expenditure and preparations for the 2022 World Cup should lead to a boost in economic activity going forward through government-mandated, large-scale infrastructure projects which would boost the construction and real estate sectors over the coming few years.

Qatar, like the rest of the GCC, is facing lower liquidity as value traded so far in 2010 has fallen over 50% versus a decline of 46% in 2009.

Oman – Positive

The outlook on Oman is Positive due to relatively healthy and sustained economic growth and positive corporate earnings. Areas of vulnerability remain in the geopolitical arena, investor sentiment and market liquidity.

Bahrain – Neutral

The report gives a Neutral outlook on Bahrain, as the economy continues to grow while corporate earnings remain healthy. Corporate earnings are expected to show a growth of 28% in 2010 due to strength in banks, but mitigated by telecom weakness. In 2011, the banking sector is expected to grow by about 28% pushing aggregate growth to 26%.The report provides an outlook for 2011 by using the six forces framework which includes 1. Economic Factors, 2. Valuation Attraction, 3. Earnings Growth Potential, 4. Investor Sentiment, 5. Geopolitical Developments, 6. Market Liquidity.

Economic Factors:

GDP Growth: According to the latest economic forecasts from the IIF, Real GDP across the GCC is likely to show a growth of 4% in 2010 followed by a growth of 4.6% in 2011; these rates remain below the historical average for the region as credit growth and private demand remain weak in some countries. Growth in Saudi Arabia is expected to increase to 4.5% in 2011 as credit growth picks up. Kuwait is expected to witness a growth of 4.4% in 2011 versus about 2% in 2010 while Qatar’s real GDP growth is expected at 18%.

Inflation: Inflation has been relatively well contained in the region as economic growth has been subdued in addition to weak real estate sectors which have brought down rents. Saudi witnessed a surge in inflation, from about 3.5% in late 2009 to 5.5% in mid-2010; however, this is expected to be sustained at that rate through 2011.

Fiscal Deficits: Fiscal balances are tightening as countries increase spending to spur economic growth; Saudi fiscal balance is expected to decline from 4% of GDP in 2010 to 2% in 2011. Kuwait, which had planned for a decline in fiscal spending in 2010, is expected to have a fiscal balance equal to 22% of GDP in 2011.

Current Account Balance: Current account balances are relatively healthy across the region’s largest economies; the highest balance is in Kuwait at 36% of GDP in 2010 to grow to 38% of GDP in 2011.

Broad Money Growth: Money supply growth has been nothing short of abysmal for the GCC in 2010; Saudi Arabia’s M2 growth has been 4% in 2010 (up to October) versus an average of 15% between 2003-2009. Kuwait has fared even worse, with virtually no growth in broad money, up just 1.8% in 2010 (November). The rest of the GCC has seen their broad money growth halve from the 5 yr average.

Valuation Attraction: Earnings weakness in 2010 pushed up PE valuations as markets remained somewhat stagnant. A resumption of healthier corporate growth in 2011 should bring down valuations.

Earnings growth is expected at 22% for 2010 (based on annualized 9M10 results). As for 2011, growth in GCC earnings is expected at 22%, which coupled with recovering markets, would bring GCC PE to about 12x, down from about 15x in 2010.

Earnings growth potential: Earnings are expected to grow another 22% in 2011 (following an estimated 22% growth in 2010) for the GCC mainly due to more stable growth in Kuwait and Saudi Arabia and a return to positive growth in Oman and the UAE.Among sectors, banks are expected to show a growth of 13% in 2010, led by a turnaround in Kuwait (growing 68% in 2010) followed by a growth of 28% as credit lines loosen and economic activity picks up across the region

Market Liquidity: Liquidity has been drying up across the GCC markets at an accelerating rate. Total value traded declined 41% in 2009 before shrinking by a further 55% so far in 2010. With an average monthly value traded of just USD 25 bn, the full year figure should be around USD 255 bn, which would be half that of 2009 (up to November 2010, GCC Value Traded is at USD 229 bn).

(For rest of the parameters and a detailed explanation of the six forces framework refer to the report online at www.markaz.com/research

About Kuwait Financial Centre “Markaz”

Kuwait Financial Centre 'Markaz', with total assets under management of over KD1.03 billion as of September 30, 2010, was established in 1974 has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997