_36.jpg)

Markaz recently released its Monthly Market Research report. In this report, Markaz examines and analyzes the performance of equity markets in the MENA region as well as the global equity markets for the month of November.

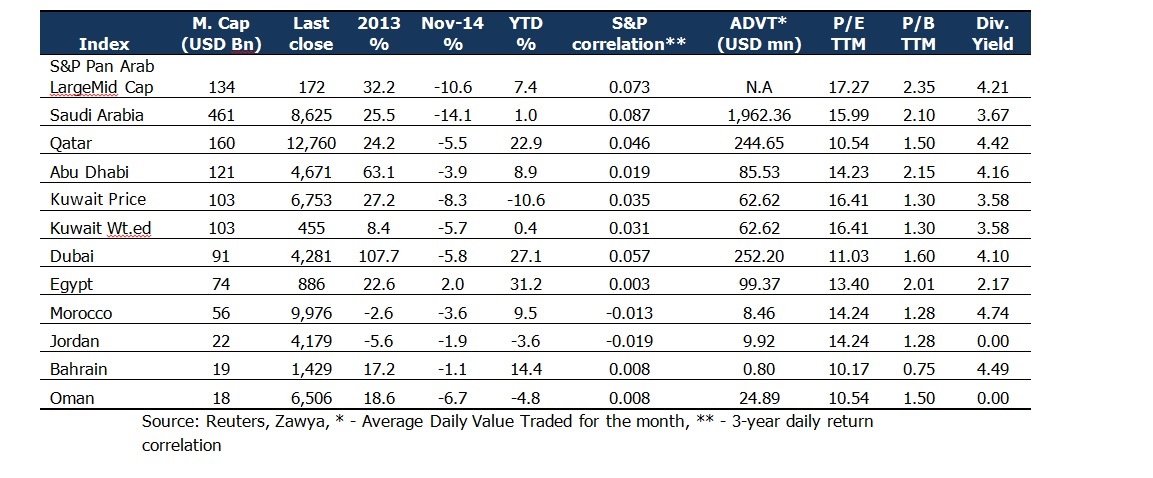

MENA Market Trends – November 2014

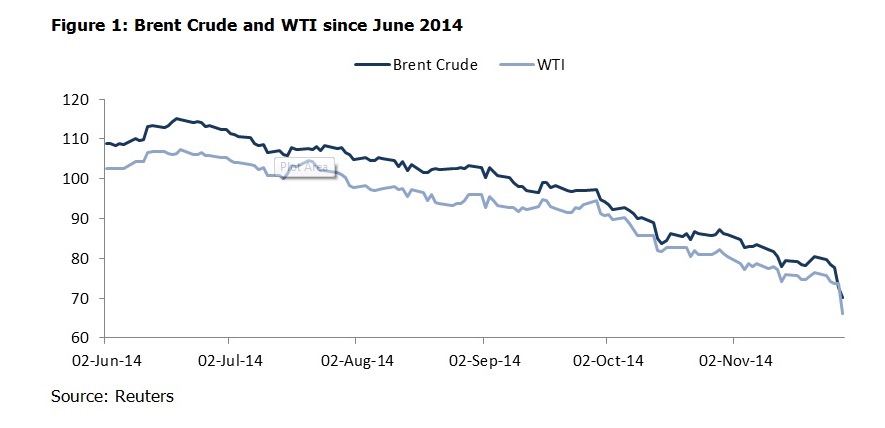

Almost all the Middle Eastern markets ended November in red, with Egypt being the only exception. Markets in Saudi Arabia (-14 per cent), Kuwait (-8.3 per cent price index & -5.7 per cent weighted index), Oman (-6.7 per cent) and Dubai (-5.8 per cent) capitulated the most. Falling oil price, exacerbated by OPEC’s decision to continue with present level of supply, has led to this fall. The Brent crude closed the month at its lowest level in four years, close to breaching the USD 70 per barrel mark. This has already surpassed, or is perilously close to the breakeven oil price of many gulf economies, and will affect their respective government’s ability to spend, despite a few nations having the luxury of accumulated oil surpluses.

The Saudi stock exchange entered a bear market as the TASI index fell by close to 4.8 per cent on the last day of the month. With OPEC continuing with current production levels, the Saudi government’s spending plans worth USD 500bn may need to be re-worked. Oman and Kuwait, both of which rely on hydrocarbon revenues for a majority of their GDP, and UAE, home to the third-largest proven oil reserves in the GCC, witnessed panic selling as investors worried about a possible slowdown in government spending, which would affect corporate earnings going forward. The southbound trend was also seen in the S&P GCC index, which closed the month at 121 points, 11 per cent lower than last month’s close. GCC countries are expected to lose over one-third of the USD 729bn oil revenues posted last year.

Egypt’s index defied political instability to post the only positive outcome for the month, closing November with a 2 per cent increase. A fall in oil price is good news for this net oil importer, and could help bridge its foreign trade gap and contain inflation.

The S&P 500, on the other hand, had a winning month, with the index climbing gradually to 2068 points, up 2.5 per cent from October. Expanding US economy, increasing consumer confidence, low and stable US interest rates, rising M&A activity, and continued monetary stimulus are cited as the reasons for the continued bull-run at Wall Street. The MSCI World Index also ended on a positive note, as markets on the other side of the Atlantic, also had a good month, despite weak manufacturing growth data from China. Chinese stock markets rose, despite weak manufacturing PMI data, as investors expected the central bank to decrease interest rates in a bid to revive activity.

National Commercial Bank, Saudi Arabia’s largest lender, came out with an IPO worth USD 6bn (SAR 22.5bn), beating the previous record held by Dubai World (USD 4.7bn). The IPO attracted up to 12.5mn investors, who pumped in close to USD 83bn, over subscribing the issue by almost 14 times, with the retail tranche alone oversubscribing 23 times.

The day they were open for secondary trading on 12 Nov, NCB’s shares jumped their daily 10 percent limit to close at SAR 49.50. The price kept soaring, reaching a high of SAR 66.50 (18 Nov), and finally ended the month at SAR 58.75, 31 per cent above the issue price (SAR 45).

Figure 1: Brent Crude and WTI since June 2014

Source: Reuters

The OPEC, which controls close to 40% of the world’s oil, has decided to leave its daily output target unchanged, failing any hope of short term price stabilization of the commodity.

The decision to continue with present production levels of 30mn barrels per day sent oil and gas companies and commodity dependent economies in a downward tizzy. Non-OPEC oil exporters, Russia, Mexico, Nigeria, Canada, and Norway, have already felt the negative effect of falling oil prices, with their stock markets heading southwards. Although US is one of the foremost producers of shale oil, it is a still a net importer, and hence benefits from falling prices.

About Kuwait Financial Centre “Markaz”

Kuwait Financial Centre K.P.S.C “Markaz”, established in 1974, is one of the leading asset management and investment banking institutions in the Arabian Gulf Region with total assets under management (AUM) of over KD 1.12 billion as of Sep 30th, 2014 (USD 3.89 billion). Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997.