_36.jpg)

If a lesson is to be learned after the two years since the outbreak of the mortgage crisis in America, it is that markets are exceedingly dynamic and not static by any means. The global economic crisis appears to have bottomed-out and it seems the worst is behind us as evidenced by recovering commodities prices with oil prices doubling year-to-date and rebounding markets having gained 20% to 60% above their troughs of last year. Government policies have materialized either as incentive packages or the nationalization of financial institutions (and sometimes, a combination of both), although recovery is imminent, it is still too early for government intervention to be withdrawn.

Although the Kuwaiti financial sector was at the heart of the crisis locally, it cannot be summed up as a battle between good (transparency and good governance) and evil (lack of transparency of companies and the mistakes of others), it extends to the private sector as well as other players including the government and economic policy makers.

Assets held by the investment sector in Kuwait almost match those of the banking sector, making it the second largest sector in the country. The huge losses sustained by the investment sector in Kuwait resulted in aggregate corporate earnings in Kuwait declining by 50% decline for the year and resulted in a 25% decline in aggregate GCC corporate earnings on an annual basis. The deadlock experienced by the sector in Kuwait is affecting the country's economy, with likely contagion to other sectors if no clear plan of action is executed.

Economic decisions have been delayed due to an attempt to democratically gather consensus in favor of government intervention, or to oversensitivity on the subject of spending national funds to bail out firms. We shouldn’t believe that we can reinvent the wheel through new solutions other than those submitted worldwide. In addition, we cannot lay the blame solely on investment managers and the risks they have taken. This report aims to shed light on the extent of the damage incurred by Kuwaiti investment companies (and their shareholders and clients) in 2008, in addition to the options available to policy makers to provide economic solutions on the one hand, and the choices faced by companies to draw lessons from the current crisis on the other.

At last the 2008 results are out

It took more than four months for Kuwait investment companies to declare their 2008 results, highlighting the difficult circumstances they were placed in, observes Kuwait Financial Centre “Markaz” in its recently released research note which aims to illustrate the current financial standing of the Kuwait Investment sector in light of turmoil in 2008 in addition to highlighting challenges facing the sector in 2009 through a stress test, and possible courses of action for investment companies.

2009 is expected to be better

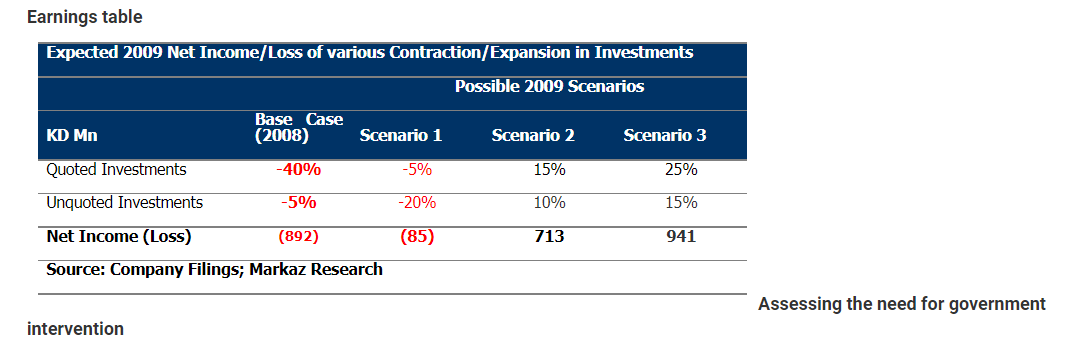

Despite the abysmal sector performance in 2008 (with a net loss of KD 892 mn or USD 3.09 bn), due to high investment losses on the back of impairment in assets, 2009 is likely to be significantly better for investment companies in the sector. Losses in 2008 were the result of a toxic combination of impaired assets (particularly illiquid assets such as private equity, real estate etc) and sharp declines in worldwide equity markets which caused contractions in quoted investments and funds.

A stress test for the investment sector

A stress test for Quoted and Unquoted Investments, which form the bulk of investment company revenues and were the root cause for losses in 2008, showed that the cumulative profits of investment companies should touch KD 713 million during 2009 as against a loss of KD 892 million during 2008. However, this would still be lower than the record profits the investment sector made during 2007 at KD 903 million.

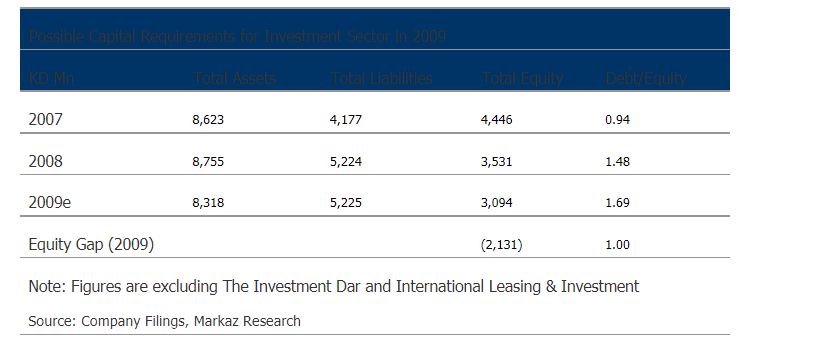

The Kuwait Investment Sector proved to be highly leveraged in 2008. Based on company filings, the investment sector had a Debt/Equity ratio of 0.94 in 2007, which shot up to 1.48 in 2008 as companies took on more debt and lost Equity on account of changes in Fair Value reserves and accumulated Losses. If the Liabilities were to remain constant in 2009, we would expect Total Equity to contract to about KD 3.09 bn, coinciding with a drop in Total Assets to KD 8.32 bn as assets continue to lose value or be liquidated in order to pay off existing debt. This would cause the sector’s debt to equity ratio to jump up to 1.70. In other words, the sector would need an Equity injection of KD 2.13 bn in order to bring the leverage ratio back to 1.00. This is a reasonable figure and well within the country’s ability to provide given the vast reserves it has accumulated in the past few years on the back of rising oil prices.

The investment sector: new realities

In light of the explosive growth in the Kuwaiti investment sector over the past few years, coupled with the severity of recent global financial turmoil and the contagion it has had in Kuwait thus far, investment firms will need to adapt themselves to the realities of the new global financial order, whereby credit/liquidity will be harder to come by and clients will demand more simplicity in products. Consequently, we see a few possible changes to the investment sector landscape over the coming years.

Business models

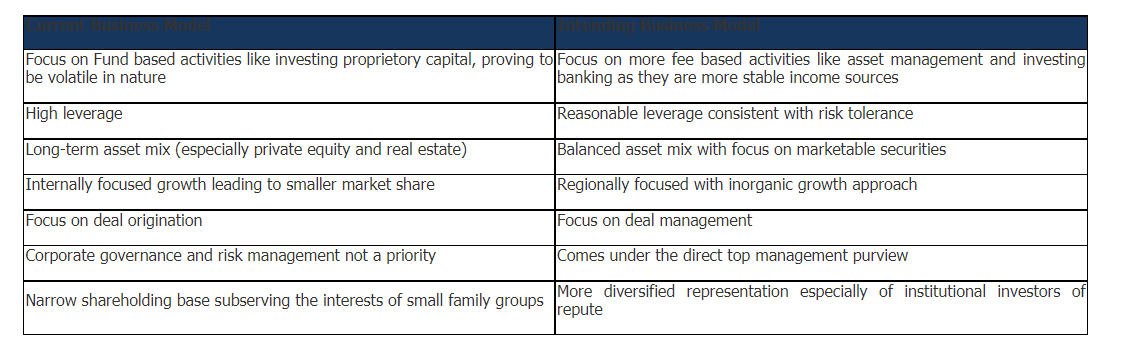

The losses of 2008 have made it clear that the current business model employed by the investment sector is highly volatile and unsustainable over the long-term. As a result, this crisis provides companies with an opportunity to alter their business models to one which emphasizes fee-based income, which is recurring and stable in nature, in addition to achieving increased diversification in their asset mix to include more liquid investments to match their shorter term Debt levels.

Consolidation presents an obvious avenue for survival in the current financial climate. The fact of the matter is that the country has an overcapacity of investment firms (100 companies) and in the coming year, we expect to see many of the smaller, weaker firms closing shop or being acquired by larger firms. Indeed, this is a healthy avenue which the government should be actively encouraging more strongly. The motivations behind M&A’s are usually to; strengthen the company’s Balance Sheet and/or increase AUM. The composition of the resulting entity is also a significant factor in M&A decisions. The current liquidity issue is another factor which will affect the M&A landscape in the next few years. Many firms wishing to consolidate may be strapped for cash, which would result in a need for more creative M&A solutions, such as Stock Swaps etc.

No need to reinvent the wheel

Government assistance, in the form of stimulus packages, lines of credit, equity injections etc have been the most visible of responses to the global financial crisis. The Financial Stability Law (FSL), which was passed as an emergency bill in late March, is an over $5 bn plan aimed at boosting Kuwaiti banks, investment companies and the economy as a whole. The plan took its own time to materialize as a law, but has yet to be implemented. The logic of government assistance, particularly in Kuwait, is irrefutable. A template for public money stimulus has been provided by countries (i.e. U.S.A. and European Union) which run fiiscal deficits, are grappling with high levels of sovereign debt and are in an overall more troubling financial and economic situation than Kuwait and yet have not hesitated to inject tax payers money into their economies and bail out ailing firms. Kuwait is not burdened with high levels of government debt (appr. 10% of GDP), does not run a fiscal deficit nor does it employ tax schemes on its citizens which would represent a road block in the use of public funds to bail out distressed firms.

Additionally, the current scenario represents an historic profit-making opportunity. Depressed asset values make government assistance fiscally attractive, by purchasing distressed assets, which have a potential for recovery or appreciation at a later date. Innovative solutions aimed at disentangling the liquidity while keeping the interests of all stakeholders in consideration, may provide significant upside to all.

Overall, the coming years are expected to be a dynamic time for the investment sector, with ample opportunities for profits by corporates and public institutions alike. Additionally, the financial crisis provides investment firms with an opportunity to restructure their business models in order to avoid being vulnerable to similar crises in the future.

Please contact [email protected] to obtain the the full 34-page report.

Kuwait Financial Centre S.A.K. 'Markaz', with total assets under management of over KD781 million as of March 31, 2009, was established in 1974 has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997; and was recently awarded a BBB+ corporate rating by Capital Intelligence Ltd.