_36.jpg)

Events in Dubai took center stage in the global financial markets for the wrong reason. The shock announcement on 25th November about Dubai Holdings expressing interest to restructure its debt sent jitters all around including developed and emerging markets. The sudden shock reaction may be the fear that this may trigger other sovereign failures. Regional CDS spreads jumped in some cases by 100% (Dubai). However, markets were quick to assess that the damage may be more localized (to GCC) and manageable.

Other than this, the global markets continued its positive performance during November with China heading the table with a MTD performance of 7% followed by India at 6%. The MSCI World posted a healthy 4.2% for the month taking the YTD to 33%. Obviously, this was backed up by some good economic news (at last) in the form of unemployment, GDP growth and home price. The performance was also helped by lower risk levels (TED and VIX). The grand performance of the equity markets are being squarely touted to weak dollar and low interest rates, both of which are expected to continue for some time.

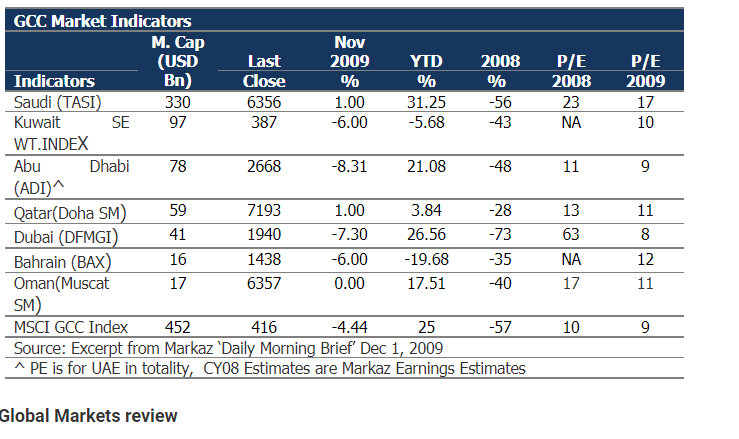

GCC markets continue to be in a mess of their own making. It lost during the month as much as the global market gained (4.4%). On a YTD basis, the GCC markets severely lag the emerging markets (25% for GCC Vs. 75% for GEM). Many reasons contributed to this including the Dubai episode. With banks and financial services still licking their wounds, earnings uptake seems to be distant dream. Gross GCC earnings fell a whopping 43% during 2008. However, the expected growth for 2009 is nearly 0%. This slowly and surely makes the markets rich in valuation and therefore poor in attractiveness. Pricing continues to be based on very thin volume leading to hyper speculation. Continued steady oil price is the only silver lining as governments may realize yet another surplus year in its budget. However, if they do not use that surplus to support and kick start investments, the impact may not get translated to stock market soon.

GCC Markets Review

The GCC markets continued to post negative returns. November marked the second consecutive month of negative returns for the GCC markets. In November, the MSCI GCC total return index posted a decline of 4.44%, this marks the highest decline since March of this year. The losses were led by the UAE markets with a decline of 14.63% (MSCI index). The announcement of Dubai holdings to restructure its debt on 25th of November had sent shock waves across the entire region during the last few days of the month. The Dubai markets in specific witnessed a 15% fall in the next four trading days. The spill over effects were significant both on the equity and the debt markets. The CDS rates spiked up for almost all the sovereigns in the region. Dubai witnessed a 99% increase in CDS rates within 3 days of announcement.

Both the volume and value traded in the GCC region declined significantly in November. The volume traded declined by 44% and the value traded declined by 36% on an aggregate for all the GCC markets on a MoM basis.

The global markets resumed its uptrend in November after a blip in October. In November, the all country world index returned 4.16%. This has increased its YTD return to 33%. However, there has been a significant decline in the percentage of markets outperforming the US markets. It has to be noted that the US market forms almost 45% of the all country world index.

The percentage of markets outperforming the US market touched a peak of 80% in July. Since then this ratio has been dipping steadily and in November it plunged to 16% from 57% in October.

This has eventually reduced the percentage share of the return from countries Ex-US in the world index. In September, 65% of monthly return was from countries other than the United States. Whereas, in November, the percentage share of monthly returns from countries other than the US has dipped to 41%.

On a YTD basis, the share of US has consistently increased over the last three months to 11% of the 33% YTD return on the all country world index.

The data releases during November point out to sequential improvement in the broad economic scenario. Firstly, the unemployment data showed the least number of jobs lost since March 2008 at -11k. Also, the seasonally adjusted unemployment rate declined by the highest percentage point since September 2006. The decline in unemployment rate was from 10.2% to 10%.

A combination of factors such as the first positive annualized quarterly GDP growth rate for Q3 at 2.78% after four consecutive quarters of negative growth, 0.4% up tick on a MoM basis in the Case shiller home price index (4th consecutive MoM up tick) and a general decline in risk levels can be attributed to the increase in US contribution to returns as compared to the rest of the world in the all country world index. The risk levels as measured by the Ted spread and Vix witnessed a decline of 1% and 13% during November on a MoM basis.

The depreciating US dollar and the low interest rates are being attributed by a few experts as the major cause for the current rally in risk assets. The trade weighted US dollar has declined by 8.5% in the YTD period and short term interest rates are currently almost equal to zero.

Among the risk assets, even commodities have witnessed a continuation of uptrend in November. The gold and Oil prices increased by 12% and 4% respectively in November alone.

YTD Market Cap Weighted returns of MSCI World Constituents

# End #

About Kuwait Financial Centre 'Markaz'

Kuwait Financial Centre 'Markaz', with total assets under management of over KD 960 million as of September 30, 2009, was established in 1974 has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997.