_36.jpg)

Kuwait Financial Centre “Markaz” has recently published a series titled GCC Sovereign Equity Risk Premium in an attempt to regularly publish the calculation of risk premium. Valuation in emerging markets is mostly considered as a futile exercise due to several difficulties which include data availability, regulatory & political risks, and a totally different capital market in terms of efficiency, liquidity, and participants. Due to the absence of financial models developed specifically for emerging markets, models which work in the West are adopted in the developing countries as well. One key input in such models is the Cost of Equity which is arrived at using the Equity risk premium (ERP).

Equity risk premium is the extra return that investors collectively demand for investing in stocks instead of holding it in a risk less investment. Equity risk premiums are a central component of every risk and return model in finance and are a key input into estimating costs of equity and capital in both corporate finance and valuation. Due to the volatile nature of equities, historical returns are not a reliable measure of equity risk premiums. It becomes doubly challenging in emerging markets where such a long history is not available. The challenge for GCC is all the more glaring in the absence of a yield curve.

Markaz research on ERP contemplates three distinct ways of calculating equity risk premium for GCC markets which can be used in valuation and capital budgeting. The method to be practiced depends really on the purpose and availability of data points.

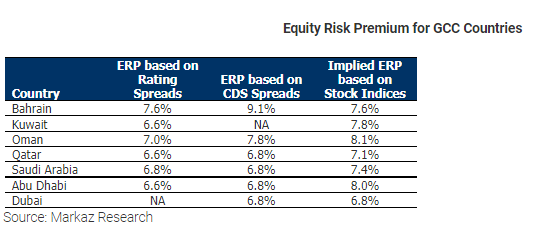

Method 1 - Sovereign Rating: Taking the latest US market equity risk premium of 6.1%[1], the ERP of GCC countries are arrived at by adding the default spread based on their credit rating.

Method 2 – Estimating ERP using CDS spreads: Rating agencies are generally considered to be slow in updating their ratings. So, instead of arriving at default spread based on rating, we can use CDS spreads as a proxy. In this method, the CDS spread of a country’s bond (adjusted for spread of risk free country) is considered as default spread instead.

Method 3: Implied Equity Risk PremiumImplied equity risk premium is an alternative approach to estimating risk premiums. Assuming that stocks are correctly priced in, if we can estimate the expected cash flows from buying stocks, then we can estimate the expected rate of return on stocks by computing an internal rate of return (IRR). Subtracting out the risk free rate from IRR should yield an implied equity risk premium. The inputs required for calculation of Implied ERP were not readily available for GCC countries. Absence of sovereign bonds for some countries made the estimation of risk free rate and perpetual growth rate difficult. Also, the lack of consensus earnings growth estimate makes it hard to determine the market’s view on growth for the next 5 years.

The results are presented in the following table.

About Markaz

Kuwait Financial Centre “Markaz”, with total assets under management of over KD903 million as of March 31, 2012, was established in 1974 has become one of the leading asset management and investment banking institutions in the GCC Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997.