_36.jpg)

Kuwait Financial Centre “Markaz” recently published the executive summary of their GCC Sector series covering Petrochemicals.

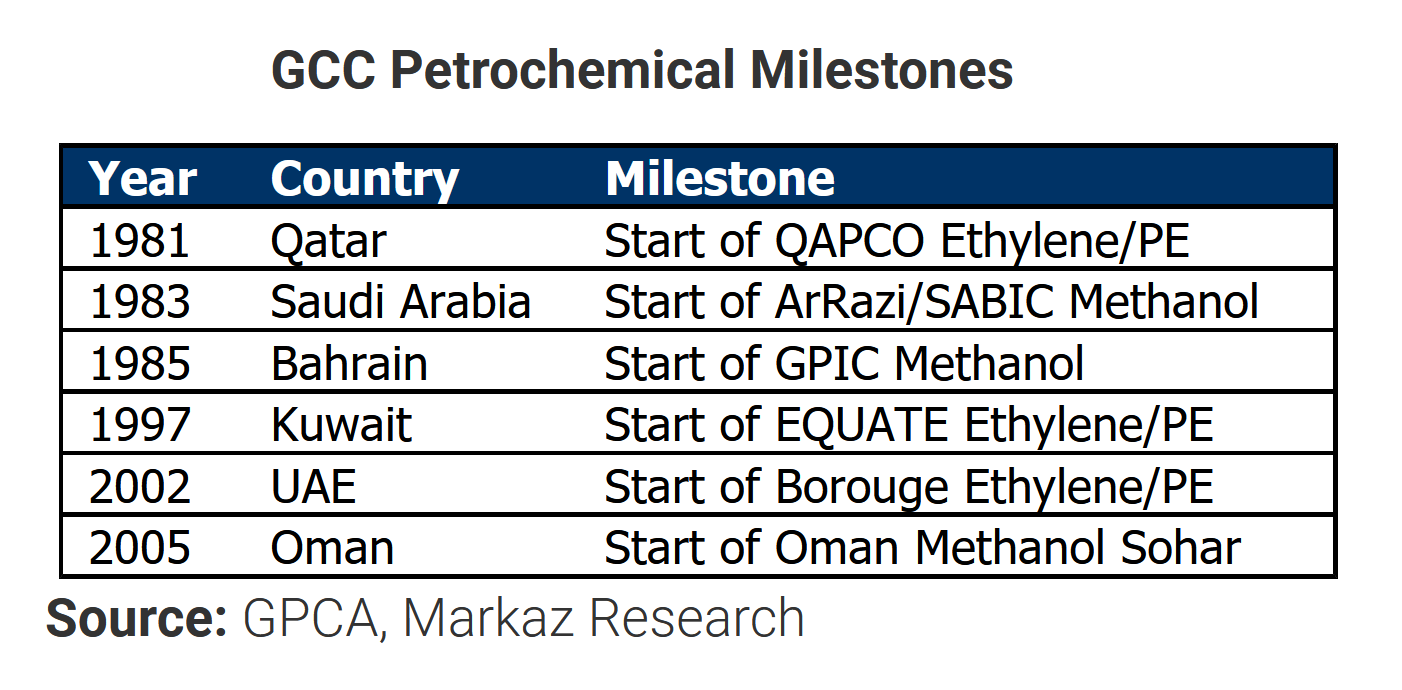

GCC petrochemical companies are amongst the lowest cost manufacturers in the world owing to cheap feedstock and energy costs. Given their strategic location and development as a major transportation hub, GCC petrochemical producers enjoy a huge competitive advantage over others.

Over the next few years, GCC countries will strive hard to prove their dominance in the petrochemical sector in an effort to diversify their economies away from Oil & Gas revenues. Development of large scale petrochemical complexes will serve the dual purpose of diversification as well as employment generation.

Petrochemical prices saw an uptrend in the first half of 2011 in line with the increase in oil prices. However, prices declined during the second half on concerns of Euro zone debt problems spiraling to other regions, which resulted in lower demand. Over the next few months, we expect prices to be under pressure due to concerns on global growth. But on a longer term, since most of the incremental demand growth is coming from emerging economies, we foresee stable prices and margins. Phasing out of older plants in the developed world and possible sanctions on Iran should augur well for GCC producers. China’s increasing self-reliance for petrochemical products is a cause of concern for GCC exporters. Sensing the risk, companies in GCC are establishing joint ventures with Chinese companies to set up integrated plants in China in order to tap local demand. But how credible this strategy is remains open to question.

Petrochemical projects worth USD 19bn are under execution in the GCC. Apart from this, projects with an estimated value of USD 81bn are in different stages of planning. Saudi Arabia tops the list with USD 12bn of projects under execution and another USD 41bn of future projects. Gulf Petrochemicals & Chemicals Association (GPCA) has estimated GCC Petrochemical Capacity to increase from 77.3 MTPA to 113 MTPA at the end of 2015. Saudi Arabia is expected to see largest capacity addition by volume and UAE will see largest growth in percentage terms.

GCC petrochemical industry is grappling with the major problem of natural gas shortage, due to increased domestic consumption in areas like electricity generation and desalination, leading to insufficient allocation of ethane to new plants. For instance, there has been no substantial new allocation of ethane for Saudi Arabian petrochemical companies since 2006.

Anti-dumping charges, levied against the region’s producers in key markets such as India and China, could set precedence for action by other countries. Even though India lifted anti-dumping duty on polypropylene imports in December 2011, there is always a risk that it will come back given the strong political lobbying. Development of Shale gas technologies, although still in a nascent stage, is being keenly watched because of the impact it may have on North American markets - which is the largest consumer of petrochemicals. If economical ways of extracting shale gas are found, US producers’ competitive position will increase after taking into account the transportation costs for GCC exports.

The Way Forward

GCC petrochemical companies must be ready to face the reality that they might not enjoy privileged access to natural gas at subsidized rates indefinitely. There is a double blow of government increasing feedstock prices for existing allocations and new projects not getting ethane allocation.

Companies should expand their current product portfolio and move into high value added downstream chain, away from basic chemicals. Apart from commanding premium pricing, such downstream products are less exposed to overall market fluctuations.

GCC governments should seriously start investing in research and development to gain technical know-how to produce specialty products. Access to homegrown technology is vital for an industry which has global ambitions.

Government’s role as a facilitator becomes extremely important for the petrochemical sector which possibly is one of the few sectors with the potential to provide large scale employment.

(For information on obtaining Full Report, please contact: [email protected])

###

About Kuwait Financial Centre “Markaz”

Kuwait Financial Centre S.A.K. 'Markaz', established in 1974 with total assets under management of over KD 865 million as of December 31st, 2011, is the leading and award winning asset management and investment banking institution in the Arabian Gulf Region. Markaz is listed on the Kuwait Stock Exchange (KSE) since 1997 under ticker Markaz.