_36.jpg)

In a recently published quarterly report by "Markaz", which aims to analyze the performance of equity funds across the region, GCC markets had a positive start to the year; after ending 2009 with a red quarter amid negative corporate news, namely Dubai World, markets swung into positives for the first quarter of 2010, led by healthier corporate earnings, stronger economic outlooks and more positive corporate news. MSCI GCC gained 12% in 1Q10 after losing 8% in 4Q09.

The quarter’s worst performer was MSCI Bahrain, which remains in the red while the best performance came from MSCI Kuwait which gained 19% in 1Q10, driven by positive news from Zain which lifted most blue chips. MSCI Saudi followed with a gain of 13% for the quarter.

GCC Equity funds had an asset weighted return of 11% for 1Q10 as fund managers took advantage of blue chip gains as local indices were carried upwards by earnings momentum and strong economic outlooks.AUM’s was just over USD 12.3 bn in 1Q10 representing an institutionalization rate (AUM/Mcap) of 1.6%. Both Saudi Arabia and Kuwait saw their AUM expand in the first quarter by 7% and 4%, respectively.

Assets under Management – March 2010

Source: Markaz Research

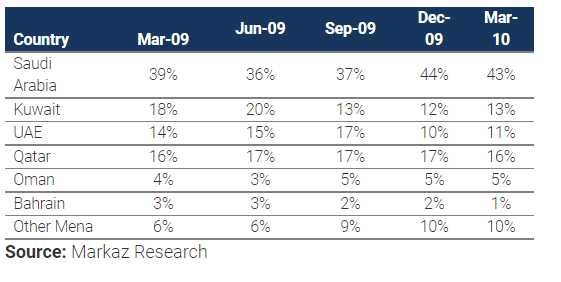

Asset Allocation Trends– GCC Equity Funds (March 2010)

Fund managers continue to favor Saudi Arabia, with an allocation of 43%. Confidence in the Kuwait market has declined, from 20% in June to 11% in March 2010; the same can be said for the UAE, where managers allocated 17% of their assets in September before cutting exposure to 11% in March.

Geographical Allocation - Equity Funds

Exposure to equities increased throughout 2009 and into 2010, with a 93% allocation in March, while Cash exposure is down to 7%, based on asset weighted average, reflecting a higher risk appetite from local and foreign investors.

Saudi Arabia Equity Funds

The Tadawul index gained 11% in 1Q10 as positive end of year results, strong economic outlook and healthy oil prices boosted the market. Banks, Agriculture and Petrochemicals led the index higher, gaining 13.7%, 13.2%, and 12.7%, respectively, for the quarter. Consequently, AUM’s expanded 7% to USD 5.08 bn.

Fund managers maintained their exposure to equities at 98% in March 2010 versus a low of 96% in June 2009, while allocation to Cash & Equivalents increased to 2% from 1% in December 2009.

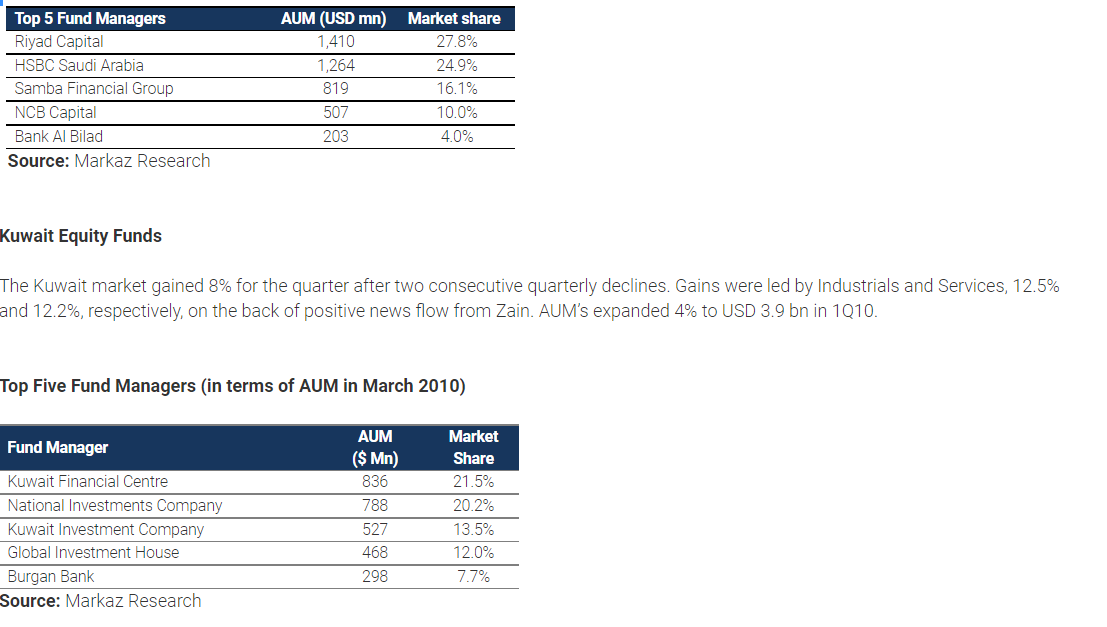

Top Five Fund Managers (in terms of AUM Mar-10)

After losing 6% in 4Q09, Qatar’s Doha Securities Market (DSM) gained 7.23% in 1Q10 led by banking, up 11.6% for the quarter after the Central Bank lifted a ban on local banks from trading on the exchange. Value traded fell 18% to USD 4.6 bn for the month.

AUM’s for Qatari equity funds were flat at USD 156 mn.

Other GCC Equity Funds

UAE Equity Funds - Dubai (DFM) underperformed the Abu Dhabi Exchange (ADX) for the quarter, gaining 2.2% versus a gain of 6% for the ADX. The DFM’s gain was led by Banking, up 5% for the quarter while Insurance and Financial Services lost 1.9% and 0.4%. Abu Dhabi’s gain was led by Telecoms, up 13.6%. Liquidity in the UAE was down; value traded declined 39% from 4Q09 to USD 10.68 bn.

AUM’s for UAE equity funds continue to contract, declining 3% in 1Q10 to USD 592 mn.

Oman Equity Funds - The Muscat Securities Market (MSM) gained 5.16% in 1Q10 after losing 3% in 4Q09. AUM’s for Omani equity funds dropped to USD 58 mn as Oman Gateway Fund was retired.

Bahrain Equity Funds - The Bahrain Exchange managed a gain of 6.1% in 1Q10, regaining the 4Q09 loss. Sectoral returns were mixed, from a high of 22% for Commercial Banks to a low of -6% for Industrials. SICO Selected Securities Fund outperformed the benchmark, MSCI Bahrain index, which lost 3.86% in 1Q10.

Kuwait Financial Centre S.A.K. 'Markaz', with total assets under management of over KD865 million as of December 31, 2009, was established in 1974 has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997.