_36.jpg)

Markaz published a report on the GCC banking sector. The authors M.R. Raghu and Layla Al-Ammar note that the year 2009 can truly be declared as a year of provisioning. The 61 banks in the GCC region are estimated to provide a whopping USD9.4 bn in provisions during 2009, a 40% jump from 2008 and a 5-fold increase from the modest level of USD 1.8 bn for 2007. As a percentage to loans, this translates to nearly 1.5% compared to 0.58% seen between 2003-2007.

The spike in some cases have been caused by specific events unrelated to the ongoing financial crisis (Gulf Bank, Kuwait and ABC, Bahrain). However, most of the story clearly points to “aggressive caution” on the part of banks to drive the bad news when the mood is gloomy. Banks are the main conduit of economic activity in the market and as such this certainly reflects the pain the overall economy is undergoing as a consequence of the global fall out. It also brings sharply into the picture the intrinsic role of credit evaluation and corporate governance standards.

A direct fallout of this can be seen in the activity levels of banks as defined by loans and deposits. Both loans and deposits enjoyed robust growth levels since 2003. The sharp drop in the fourth quarter of 2008 was not enough to contain this where loans experienced a growth of 34% and deposits 21% during 2008. However, the picture took a nasty turn in 2009 with overall loan growth at an anemic 4% weakly supported by a deposit growth of 3%. We expect a slight pick up in 2010, but no where near the historical average.

Within the GCC, the focus at the end of 2008 was on a myriad of things; the UAE Real Estate sector, the Kuwait Investment sector, not to mention hemorrhaging stock markets across the board. A lesser discussed topic was the GCC banking sector, which the majority of Central Banks and Monetary Authorities deemed as healthy and stable at the onset of the crisis except for a few episodes.

Banks made slight increases to their provisions across the board in 2008; however, pivotal in moving the overall GCC needle were provisions of over USD 1 bn from both Gulf Bank of Kuwait and Bahrain’s Arab Banking Corp, over USD 700 mn from Kuwait Finance House and nearly USD 500 mn from Emirates NBD.

That was 2008, where the GCC-wide increase in provisions could be attributed to a handful of the largest GCC banks… what about 2009? 9M 2009 figures show that provisions have increased almost without exception across GCC banks, i.e. not just the “big guys”. GCC Provisions for 9M09 have already topped USD 6.41 bn, or 1.06% of loans.

By far the most volatile has been the UAE, following the announcement of debt woes at the two Saudi conglomerates, Saad and Algosaibi Groups, which UAE banks are believed to have a significant amount of exposure to (estimated at over USD 2 bn), the central bank has charged all banks with taking provisions amounting to 50% of their exposure to the troubled groups. Additionally, news concerning the debt woes of Nakheel, and its parent firm, Dubai World, have heightened the sense that more trying times are in store for banks going forward. Consequently, UAE provisions doubled in 2Q09 to over USD 1 bn; total provisions for 9M09 stand at USD 2.57 bn and we would expect this to near the USD 4 bn mark by year end and to increase to USD 4.8 bn in 2010, especially should lending continue to be tight while banks continue to guard against defaults.

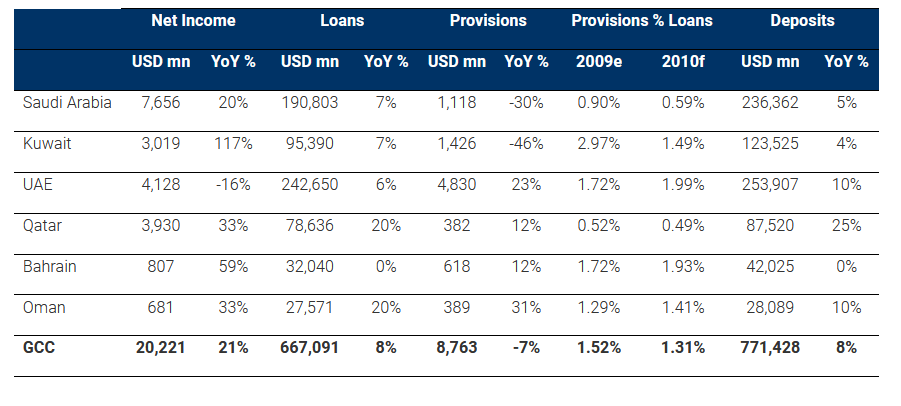

We expect GCC provisions to end 2010 at USD 8.76 bn, representing a 7% decline over our full year 2009 estimated provisions of USD 9.4 bn. Concurrently, lending activity stagnated across the GCC in 2009, with growth rates falling well below historical averages, as banks have hoarded cash and been hesitant to extend financing in a tenuous economic environment. GCC loans have amounted to roughly USD 606 bn in 9M09, a 5% growth from the same period in 2008. Saudi Arabia has been the main drag on loans growth, growing just 1% in 3Q09 compared to 3Q08, in stark contrast to the 25% average growth in loans seen in the last five years. We expect GCC loans to show an overall growth of 4% in 2009, a far cry from the historical average of 29% between 2003-2008. This would bring the provision to loans ratio to 1.52% in 2009 as compared to 1.13% in 2008. While we expect to see some recovery in lending in the GCC, we still expect Saudi Arabia and the UAE to be a drag on overall GCC loans growth. Hence, we have a forecasted 2010 loans growth of 8% for the GCC to USD 667 bn.

Summary 2010 forecasted Performance of GCC Banking Sector

Source: Reuters Knowledge, Markaz Research

###

About Kuwait Financial Centre “Markaz”

Kuwait Financial Centre S.A.K 'Markaz', with total assets under management of over KD 960 million as of September 30, 2009 was established in 1974, and has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997.