In a perfect world, all investors would take logical decisions with the markets being priced to perfection. However, this is far from the reality as most investors are much less rational than they think when it comes to decision making. Their irrationality does not relate to a lack of ability, but purely reflects the fact that humans tendto be driven by emotions. These emotions govern everyday decision making of individuals, giving rise to certain biases. When these biases come across to the world of investing, they result in inefficiencies that end up costing investors dearly. Especially during crisis situations, when investors are stressed and resort to panic, even the most logical minds fall back to making the basic mistakes which we would otherwise not make. Therefore, at this juncture where

markets have come crashing down, investors need to be wary of some biases that could potentially result in huge financial losses.

1. Loss aversion

Loss aversion suggests that for individuals the pain of losing is psychologically twice as powerful as the pleasure of gaining. In simpler terms, the feeling of fear is much more powerful than greed. When investors see their portfolio value falling by the day, they tend to hit the sell button prematurely to avoid further losses and invest when times are better.

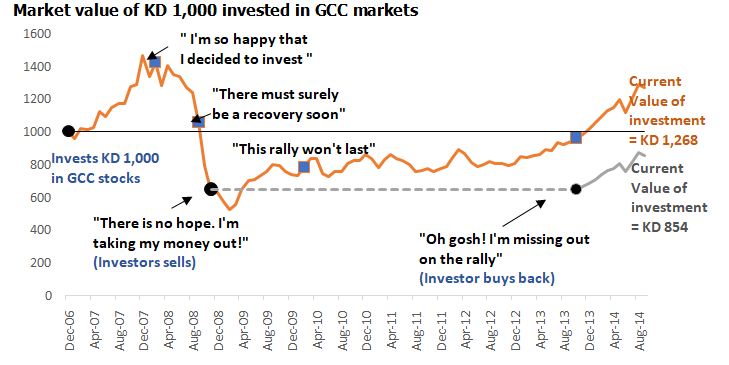

Source: Marmore Research, Reuters; Note: MSCI GCC index is used, KD 1,000 is invested on Dec 31, 2006 close.

Investment value of KD 1,000 if the investor stayed invested; Investment value if the investor sells during downturn and reinvests when there is a rally

The above example shows that an investor who tends to stay invested ends up with greater returns than that of an investor who panic-sells in the midst of a crisis and invests later.

Takeaway – Do not panic! Markets tend to have cycles. Stay invested for a long term.

2. Recency Bias

Recency bias is the tendency of investors to focus on recent events and extrapolate them into the future.In the process, they tend to forget what happened prior to these recent events. Ignoring information that is old and placing too much emphasis on recent information is one of the biggest mistakes that investors make quite often. When a portfolio’s yearly return is negative during a year, they tend to forget its performance in previous years and expect it to fall further in the next year.

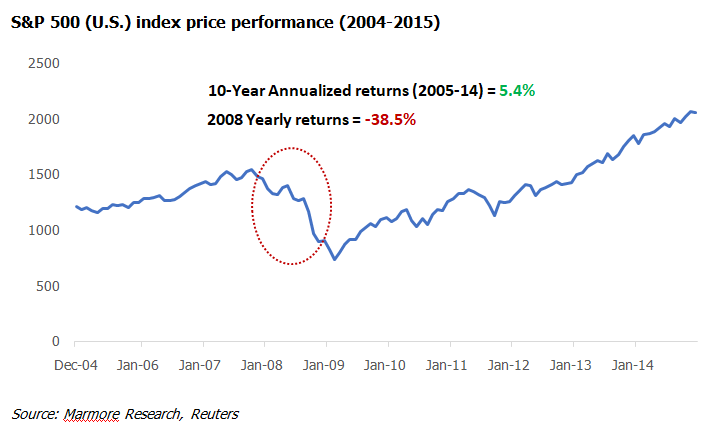

In the above example, U.S. markets had a negative return of 38.5% in 2008, but later bounced back. The 10-year CAGR returns between 2005 and 2014 was 5.4% despite the crisis, suggesting that in a longer time horizon, markets tend to recover and give positive returns. If an investor took out their money after the 2008 meltdown, they would have missed out on the rally that followed. Therefore, guessing the market direction based on recent events would not be a sound strategy.

Takeaway – Do not let recent performance affect your investment decisions. Invest systematically for a longer term.

3. Overconfidence Bias

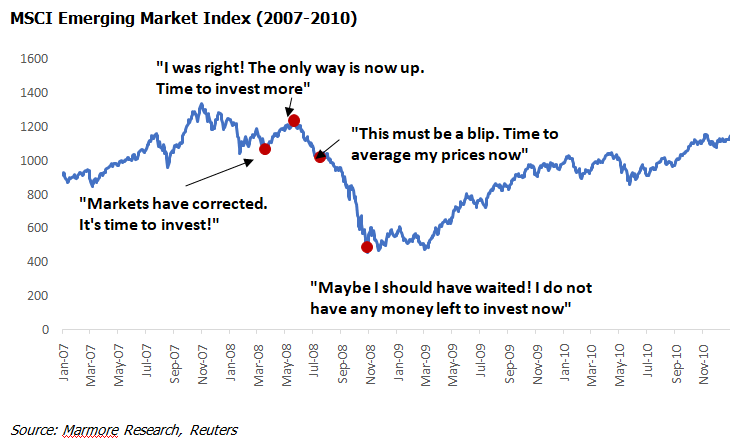

Overconfidence bias is the tendency to hold a false and misleading assessment of our skills, intellect, or talent. In short, it’s an egotistical belief that we’re better than we actually are. It is a common thought among fund managers that their performance is either average or above average when compared to passive indices as they believe that they have the ability to assess the market better and take decisions instead of following an index blindly. However, the majority of fund managers fail to beat benchmark returns. The case is similar for most individual investors who believe that they have the ability to time a market. The belief that they could predict the trajectory of future events correctly is a fallacy that results in many investors losing their money. In hindsight, it is easy to point to a level and say that it was the market bottom, but it is close to impossible to predict so with great confidence when we are experiencing it.

Certain investors overestimate their ability and end up making irresponsible investment decisions, which they regret later. Their rational thinking does not hold good at certain times as the ability of markets to stay irrational for longer periods is higher than the ability of investors to stay liquid. Therefore, it is always smart to adopt a wait and watch approach.

In the above example, there are many instances where intermittent rallies have been bought into by investors. In most cases, they have been led to further declines. As investors tend to jump in earlier than necessary based on their beliefs rather than facts, they tend to get trapped, losing their liquidity and being unable to invest at the right moments.

Each crisis is a lesson, but it doesn’t necessarily mean that all crises follow the same pattern. Biases are inherent for humans by nature and could be avoided with utmost discipline. Alternatively, these biases could be removed by eliminating the human aspect during decision making. Robot advisory platforms that use Artificial intelligence and complex algorithms could be the way to go in the future to avoid biases.

Takeaway –Do not try to time the market! Each crisis is new and might play out differently. Tread with caution and wait for a sustained recovery before investing rather than trying to catch a falling knife.