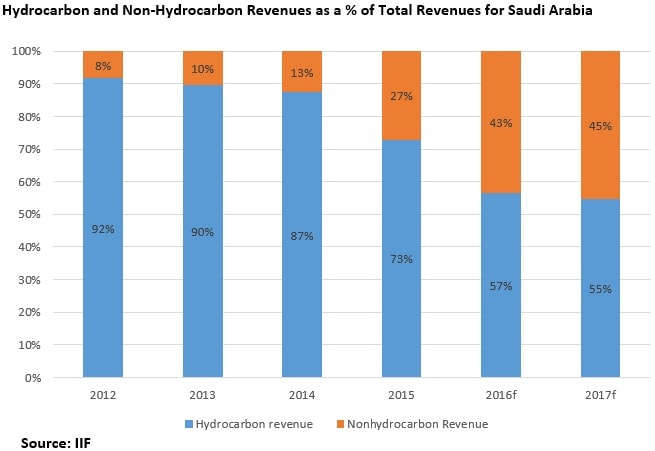

Saudi Arabia seems to be in a hurry to reform its economy and capital markets. It is not without reasons. Low oil prices have resulted in Saudi Arabia burning through its reserves at a record pace. Saudi Arabia’s foreign exchange reserves peaked during the third quarter of 2014 reaching USD 754 Bn just before the oil prices started their plunge. Saudi Arabia lost close to $160 Bn in revenues in a matter of 18 months. Its GDP is heavily skewed on oil accounting for close to 44% of the GDP which poses a problem as oil price drops. IIF projects non-hydrocarbon revenues as a % of total to increase from 8% in 2012 to 45% in 2107 on account of low oil price and announced reforms.

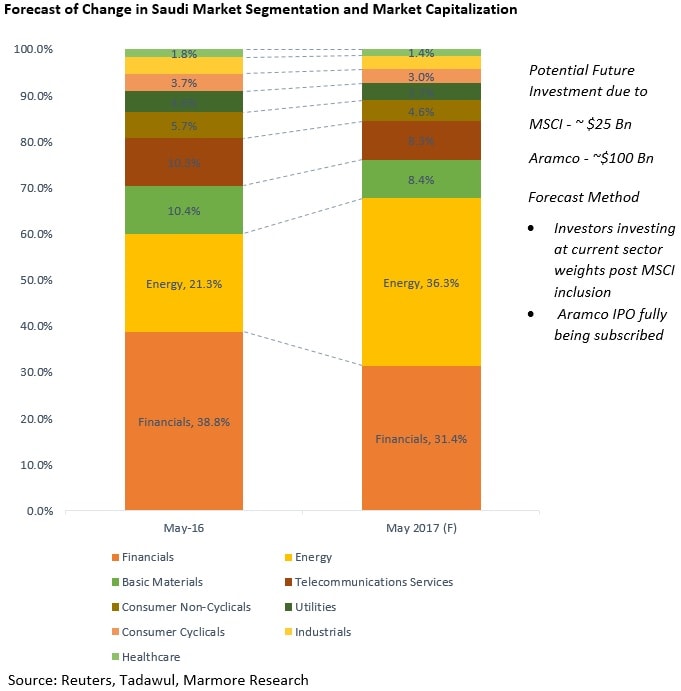

The Tadawul All Share Index plans to increase the listings to 250 companies from about 170 now, over the next seven years. Its current market capitalization of $396 billion is expected to add close to $ 120-130 bn post the IPO of Aramco and possible inclusion into the MSCI emerging market index by Mid-2017. The aim of the government is to increase the size of Saudi Arabia’s stock market to match that of its GDP within seven years (2014 -$798 Bn) as part of the vision 2030 statement released by the country’s crown prince. Another aim of the government is to make the stock market a better representative of the economy. Currently Financials dominate the stock market capitalization accounting for 39% of the stock market with stocks in the energy segment accounting for 21% of the market. In terms of GDP however the share of energy companies is double that figure at close to 40%. We have tried to find out the changes that both these events would have on the distribution of the stock market capitalization.

Large-scale infrastructure spending combined with the currency peg and the necessity to finance budget deficits means that the Saudi Arabian government should look at alternative means of increasing its income. IMF (The International Monetary Fund) warned in October 2015 that Saudi Arabia could run out of financial assets by 2020 if the government maintained its current policies and spending patterns underscoring the need to shore up public finances.

In a recent announcement, Saudi Arabia announced a string of reforms to its capital market that could attract billions of dollars of foreign money and smooth sales of state jewels – for instance Saudi Aramco. There were three major changes that were introduced in the Saudi capital market – Increased foreign ownership, Securities lending and Short Selling.

- Individual foreign institutional investor will be allowed to own a stake of just under 10 percent of a single listed company, up from a previous ceiling of 5 percent. Currently only Saudi British Bank and Banque Saudi Fransi are the two companies that have more than 5% foreign holding which are promoters’ holding of HSBC and Credit Agricole respectively.

- All foreign investors combined will still be limited to owning 49 percent of any single firm.

-

Top companies (by M.Cap) - Foreign Holdings

- This would increase the institutional investors investing the market. Single QFI (Qualified Foreign Investor) could hold onto a higher percentage of a company’s share possibly opening opportunities for higher corporate governance related disclosures, trading volumes and analyst coverage.

- Removal of the 10% ceiling on combined ownership by foreign institutions of the market's entire capitalization. Since its opening last June the total direct and indirect foreign investment accounts for close to 4.28% percent of the stock market capitalization according to Tadawul as of 26th May 2016.

- Reduction of minimum assets under management to USD 1 bn instead of USD 5 bn.

- Allow new type of foreign institution including Sovereign Wealth Funds (SWFs) and University Endowments. Currently there are 9 QFIs who have registered with the Saudi CMA (Capital market Authority) for investing in the stock market.

Other changes that were introduced included – introduction of securities lending, covered short selling and extending the settlement of trades to the globally followed standard of T+2 days instead of the current T+0 days. The T+0 days had put lot of foreign investors in trouble as they had to settle the trade within the day which required huge amount of capital to be ready before trading. Also, given the Sunday - Thursday business week, things get even more complicated. Securities lending and short-selling would help in price discovery helping in better efficiency in the market.

Possible Impact of these regulations

Increase in foreign Ownership

- Increased Foreign investment

- Increasing foreign investment is prime objective of opening up the stock market which would further enhance the appeal of stock market to sophisticated HNWIs of the region.

- Taking the top 20 stocks alone, if foreign investors increase their shareholding by 5% we could expect $13 Bn to enter into the market. However, assuming immediate investments from foreign investors may be premature. Refer to the analysis below to get a better understanding (Market Opened - Where are the foreign investors?).

- Improved shareholder protection and disclosure –

- Foreign Investors would require a robust framework to be present in order to invest into the country. While increasing the investment limit is only part of the story, ensuring equal rights for foreigners would assure them of a legal recourse

- The Dubai Financial Market General Index doubled in the two years since the news of the MSCI upgrade was announced in June 2013.

- Institutional investment is bound to add more liquidity supporting measures by constantly trading in these stocks

- Sophisticated foreign investors would make the market more efficient which would dampen knee-jerk reactions from the stock market during turbulent economic times

- Analysts from the Saudi Arabia and other GCC countries would start covering Saudi stocks more as foreign investors start to look for alpha stocks outside of the index

- Possible improvement in market cap as well as volumes/value traded

- Diversified Institutional Investor base

- Improved analyst coverage

- Improve corporate governance practices

Securities lending

- Higher Liquidity

- Securities lending is a practice that has helped developed markets achieve higher liquidity by prompting short-sellers to be more active in the market

- Price discovery

- More number of sellers due to short selling which ensures lower bid-ask spread – Bulk trades influence the markets – Upward price movement of 0.5% for block purchases and downward revision of -0.38% for block sales according to Price Impact of Block Trades in the Saudi Stock Market working paper prepared by Ahmed A. Alzahranai, Andros Gregoriou, Robert Hudson and Kyriacos Kyriacou

- Opportunity for earning by loaning out the securities which could lower the cost of holding for institutional shareholders

- Required for covered short-selling

- Derivatives have not been able to make much of inroads into the region hitherto which could increase the depth of KSA’s market

- Could open up opportunities for derivatives trading

Settlement of Trades

- Less capital needed upfront as settlement can take two days instead of the current cycle of T+0

- Possible inclusion into MSCI index

- T+0 settlement was cited as an hindrance in MSCI’s Saudi Arabia market accessibility review removal of which should help Saudi Arabia gain a place in MSCI’s emerging market index

The exact timeline for the implementation of these measures would only be known by 1st half of 2017. Lengthy time consumed for reforms to materialize could be a deterrent for overseas funds and foreign institutions from bringing their money into Saudi Arabia. Since June 2015, the total direct and indirect foreign investments account for 1% of the USD 408 Bn Saudi stock market. As of December 2015, there were only nine foreign institutions that had registered in Saudi Arabia as foreign institutions.

Market Opened - Where are the foreign investors?

Saudi Arabia opened up its markets to investors during June 2015 following the announcement in 2014. Liberalizing the stock market, one of the few major global exchanges to have restricted foreign access was expected to attract a huge amount of foreign investors. However the expectations failed to materialize which resulted in the stock market falling on the day that foreign investors were allowed to trade. Primary reasons for the poor show on the day of market opening were two – Initially, Foreign Institutions that had applied for license did not get them on time and stock market valuations were on the higher side compared to regional markets. The situation continues to persist with foreign holdings not seeing any major improvements. QFI holdings remain below 1% for many large cap stocks.

Rich valuations play spoilsport – When the stock market opened up to investors last June it was already the region’s top performer returning 15% (As of June 2015) and trading at a PE of 15.5 times its 12 month forward earnings. In comparison the broader Middle East market were trading at a multiple of less than 14 times earnings while global emerging markets were trading at 11.9 times. Saudi Arabia is not part of MSCI EM index and currently features as a standalone market closing the doors for passively managed funds. Actively managed funds as opposed to passively managed funds are very choosy about their investments and would only invest if the returns are expected to be commensurate with the level of risk. Investor sentiments were further dampened by the deteriorating economic conditions in Saudi Arabia due to decline in oil prices. Banking sector which form the majority of the market cap was worst affected.

QFIs shareholding remains well below 5% - What is the point in changing it to 10% - Some analysts also point out that this was more of a measured opening to help foreign investors get a feel of the market and for Saudi Arabia to adjust itself to foreign investors. Recent reform announcements suggests that Saudi Arabia is serious about bringing in foreign investors and getting into indices provided by MSCI (particularly EM Index) and FTSE. On successful inclusion more foreign investment can be expected to reduce tracking errors of foreign funds tracking such indices.

How will the market segmentation look like in 2017?

There is a significant difference between the composition of GDP and the stock market segmentation (by market capitalization). Decision on Saudi Arabia’s inclusion into emerging market index is expected to be taken by MSCI by Mid-2016 and possibly addition into the index would happen by mid-2017 with an initial country weightage of 2%. We look at how this can affect the sector composition of Saudi Arabia’s stock market.