_36.jpg)

GCC stock markets significantly underperformed the emerging markets during 2009. As against a 74% increase in emerging markets during 2009, GCC market returned a pale 18%. Surprisingly oil prices remained strong throughout 2009 with a YTD increase of 85%. A recent report released by Kuwait Financial Centre “Markaz” points out that the financial crisis of 2009 laid bare the fragilities of the GCC stock markets. While market specific bad news was mainly responsible for the lackluster performance, lack of progress in regulatory structure (a key determining factor for attracting credible foreign money), and steep fall in liquidity (value traded) added to the woes. Earnings destruction was significant to recoup within a short span of time. Asset quality impairment for banks revealed the overall economic weakness and corporate governance failures came to the fore.

The report notes that in the past a strong oil price was enough to lift the market to speculative heights. Money was easy to make in that environment with north being the only direction where the price of any stock could move. Transparency and research was never demanded (due to lack of institutional investors) and even when demanded, they were not heeded to. However, in the “new normal” world, oil price is not the only variable affecting the fortunes, hence, the relevance of the report’s 7-force framework.

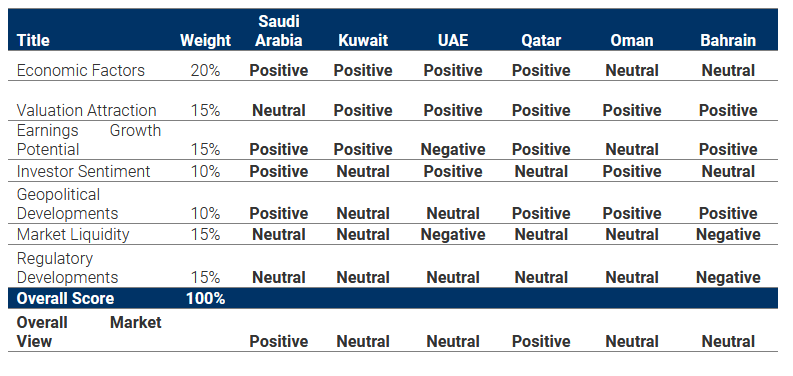

When looked at the markets with this prism, a bullish outlook is given for Saudi Arabia and Qatar while being neutral on all other GCC countries.

Country Views

Saudi Arabia – Positive

The report maintains a positive outlook on Saudi Arabia driven by strong positive economic expectations, healthy corporate earnings, positive investor sentiment and a stable geopolitical structure. Pockets of neutrality exist in terms of valuations (PE), market liquidity and regulatory structure.

Economically, the Kingdom is expected to resume growing at 4% in 2010 (in line with the historical average), while inflation is expected to remain under control. Healthy crude oil prices are expected to have a positive effect on the fiscal and current balances. As for corporate earnings growth, these are expected at 14% for 2010 versus an estimated 26% in 2009. In terms of sectors, corporate earnings support is expected to come from Banks and Financial Services. Additionaly, investor sentiment (as measured by Bayt.com) was up 12% YoY as of August 2009 while the geopolitical outlook (as measured by EIU) remains stable.

Market liquidity remains a concern for all GCC markets; in the Kingdom, value traded was down 35% in 2009. However, the market is fairly open to foreign investors and the regulatory structure is relatively sound.

Kuwait – Neutral

The authors revised their outlook on Kuwait from Positive (in September 2009) to Neutral for 2010. While the country’s economic and corporate earnings outlook remain positive, the distress in the investment sector and lack of concrete positive triggers may hamper. Investor sentiment is low at the moment with lakcluster trading.

Kuwait’s economy is set to resume a growth rate of 3.3% in 2010, about half the historical average, while inflation is likely to remain under control. Healthy oil prices and low fiscal spending will produce healthy fiscal and current account balances in the coming year. On the corporate earnings side, Kuwait is expected to lead in terms of growth in 2009 due to a solid turnaround expected in investment companies. Overall earnings are expected to grow by almost 5x during 2010 primarily due to extraordinary destruction in earnings during 2009.

UAE – Neutral

A Neutral outlook is maintained on the UAE given the mixed signals in the country; the economic outlook is positive with a 3% GDP growth expected for 2010 while investor sentiment remains fairly positive. Additionally, the geopolitical and regulatory arenas are considered to be stable.

On the other hand, corporate earnings look negative for 2010, with an overall decline of 9% expected for 2010 after an estimated decline of 26% in 2009. The financial services, banks, and real estate sectors are expected to drag overall earnings, with annual declines of 21%, 16%, and 15%, respectively, forecasted in 2010. Telecom is the only sector expected to post positive earnings growth in 2010, to the tune of 10%.

Qatar – Positive

The authors revised upwards their outlook on Qatar, from Neutral to Positive, on the back of good economic and corporate earnings.

Qatar’s GDP is expected to grow at 18% in 2010 coupled with positive fiscal and current balances. Corporate earnings are expected to show an overall growth of 15% in 2010, after declining an estimated 3% in 2009. The Banking and Telecom sectors are expected to boost overall earnings, with 2010 growth rates of 33% and 15%, respectively.

Pockets of concern in Qatar are with market liquidity as value traded declined 46% in 2009 after increasing 57% in 2008. Moreover, lower investor sentiment and a slightly ambiguous regulatory structure remain of concern.

Oman – Neutral

The report revised downwards the outlook on Oman, from Positive to Neutral, due to decelerated economic growth, moderating corporate earnings outlook and low market liquidity.

Bahrain – Neutral

The authors revised upwards their outlook on Bahrain, from Negative to Neutral, as positive stimulus comes from corporate earnings. Corporate earnings are expected to grow at 51% in 2010 following an estimated growth of 9% for 2009. Financial services are expected to remain a drag on overall earnings but a forecasted 59% growth in Bank earnings is expected to boost overall earnings.

The report provides an outlook for 2010 by using the seven forces framework which includes 1. Economic Factors, 2. Valuation Attraction, 3. Earnings Growth Potential, 4. Investor Sentiment, 5. Geopolitical Developments, 6. Market Liquidity, and 7. Regulatory Developments.

- Economic Factors: GDP Growth: According to latest economic forecasts, Real GDP across the GCC is likely to show a contraction of 0.1% in 2009. Economic growth is expected to resume in 2010 with GCC real GDP growing at 4.2%. Following negative growth in 2009, Saudi Arabia, Kuwait and the UAE are expected to see real GDP growth of 4%, 3.3% and 3%, respectively, in 2010. For Saudi Arabia, this would mark a return to the average growth seen between 2000-2008; however, it remains sub-standard growth for both Kuwait and the UAE. Kuwait and the UAE are expected to have the lowest growth rates in 2010 while Qatar is expected to forge ahead with a 2010 Real GDP growth of 18.5% following an estimated 11.5% growth in 2009.

Inflation: Inflation is expected to continue to decline in 2010 for most of the GCC economies, except for the UAE and Qatar where consumer prices are expected to increase 2.5% and 4%, respectively.

Fiscal Deficits: In 2010, Bahrain is expected to post a fiscal deficit of -2% of GDP while the remaining GCC nations are expected to have another year of surpluses, the highest being Kuwait, where a decline in fiscal spending is expected to push the fiscal surplus to 33% of GDP in 2010.

Current Account Balance: Current account balances as a percentage of GDP are expected to recover across the board. The largest gain is expected in Kuwait with a 2010 current account balance equal to 32% of GDP.

Broad Money Growth: Money supply growth slowed noticeably in 2008, and has decelerated further for most of the GCC in 2009. Qatar’s money supply grew 13% YoY in 3Q09 while Bahrain remains flat. Kuwait’s M2 grew 16% YoY in October 2009.

- Valuation Attraction: In 2009, valuations increased to double digits due to a combination of some price appreciation and weakening earnings growth. Earnings growth is expected at 6% for 2009 (based on annualized 9M09 results). As for 2010, GCC earnings are expected to grow 16% in 2009, which would bring valuations down to low to mid double digits. The exception to this is Saudi where 2010 PE is expected at 18x up from 13x in the last outlook report due mainly to price appreciation.

- Earnings growth potential: On the corporate earnings side, by annualizing the 9M results, the report sees a 6% earnings growth rate for 2009. Kuwait is expected to lead in terms of growth in earnings for 2009 due to a solid turnaround expected in the investment companies. Earnings in Kuwait are expected to grow by almost 5x as compared to 2008. For 2010, a bottom up approach shows a 16% growth in earnings for GCC as a whole as compared to 2009. Among the sectors, the report expects strong earnings growth rate in the financial services sector segment due to the significant contraction witnessed in 2008 and a small revival in 2009.

- Market Liquidity: Continuing a declining trend which started in 2007, total value traded dropped 41% to USD 511 bn in 2009, after declining 14% in 2008. The declining trend is driven by the Saudi Arabian bourse, which shed 35% in 2009. All markets saw their value traded decline for the year, the largest of which was a 62% drop in Bahrain. Liquidity in the UAE fell by 54% to USD66.7 bn.

(For rest of the parameters and a detailed explanation of the seven forces framework refer to the report online at www.markaz.com/research)

###

About Kuwait Financial Centre “Markaz”

Kuwait Financial Centre S.A.K 'Markaz', with total assets under management of over KD 960 million as of September 30, 2009 was established in 1974, and has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997.