_36.jpg)

Returns in April showed signs of significant momentum. GCC markets posted a 7.94% return in March and in April the momentum continued and the markets posted a return of 16.83%. All the GCC markets posted positive returns in April. Five of the six GCC markets posted returns in excess of 10%. Saudi Arabia led the gainers with a return of 20.8%. In March, due to the reversal in trend, the momentum model was overweight on all the markets, due to which it was leveraged by 20%. This had led to significant out performance of the model as compared to the SAA. The out performance for the month of April was at 3.32% and for the year at 6.46%.

Similarly, in the case of emerging markets and the world indices, the trend of momentum continues to be strong post the reversal in March. The MSCI world index increased by 11.9% after posting a gain of 8.29% in March. The MSCI emerging market index too increased by 12.8% after posting a return of 10.4% in March.

The volatility levels continue to be lower as compared to the recent peak witnessed in November 2008. However, on a MoM basis, there has been an increase in volatility for five of the seven markets (ADSM and DFM are counted as two different markets) in the GCC region. Among the developed and emerging markets, the volatility levels continue to witness a decline.

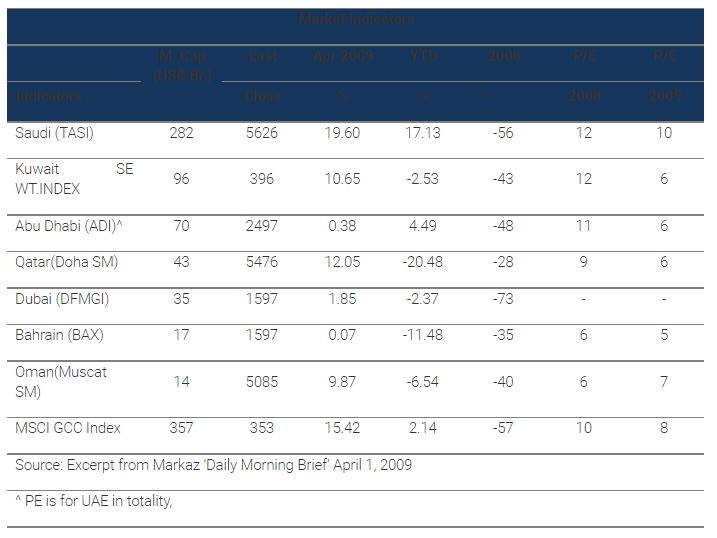

Market Indicators

Volatility (as measured by the Markaz Volatility Index)

Volatility levels continue to be lower than the recent historic peaks witnessed in Oct/Nov 2008. For the Ex-GCC indices such as the S&P 500 and MSCI EM the volatility levels are down by 58% and 65% respectively from their recent peaks in 2008. MVX for individual markets such as India and China have also witnessed declines by 56% and 57% respectively.

For the GCC region, the MSCI GCC index is lower by 26% from its recent peak. However, majority of the markets ex-Kuwait and Qatar has witnessed increases in volatility levels in April on a MoM basis. Bahrain which posted a continuous decline in volatility levels from Sep-08, witnessed its volatility levels increase by almost 2x in April alone.

Comparable MVX Levels as of April 30, 2009

Source: Markaz Research

Saudi Arabia

Saudi Arabia’s Tadawul All-Share Index (TASI) surged 20% in April after gaining 7.28% in March.

The Tadawul’s gain was led by the Al Rajhi Bank and Samba, which gained 37% and 34%, respectively, for the month.

For March, the total volume and value traded stood at approximately 4.9 Bn and USD23.34 Bn, respectively, an MOM decrease of 9% and 14%, respectively. Concentration of the top five stocks in terms of volume and value traded to total market capitalization stood at 19%.

Kuwait

The Kuwait Index gained 11% in April, slightly higher than its March gain. All sector indices were up, the month was led by Real Estate, Industrial and Services, which gained 17.7%, 17.3%, and 10.4%, respectively.

The total volume traded in Kuwait surged by 93% in April to 15.5 bn shares, while total value traded spiked 96% to USD 9.8 Bn in the same month. Concentration of the top five stocks in terms of volume and value traded to total market capitalization stood at 2% and 24%, respectively.

United Arab Emirates

The UAE markets ended the month on a positive note; the Dubai Financial Market (DFM) gained 2.36% while the Abu Dhabi Exchange (ADX) gained 1.55%. On a market cap weighted basis, the markets were flat. Dubai’s gain was boosted by 16.8% and 11% gains in Investments and the Real Estate sectors while Banks fell 6%. Abu Dhabi’s gain was boosted by Banks, which were up 8.5% while Insurance dipped 3.07%.

The total volume traded in UAE increased 32% to 15.3 Bn, whereas the total value traded was up 43% to USD 5.5 Bn in April. Concentration of the top five stocks in terms of volume and value traded to market capitalization was 9% and 13%, respectively.

Qatar

The Doha Stock Market (DSM) was up 12% in April after gaining 10% in March. Gains on the DSM were led by the Services and Banking sectors, which gained 25.5% and 12.6%, respectively, in the month.

In April, total value traded on the DSM declined 2% to equal USD 2 Bn while total volume traded was down 4% to 306 mn. Concentration of the top five stocks in terms of volume and value traded to market capitalization was 13% and 38%, respectively, in April.

Oman

The Muscat Securities Market (MSM) gained 10% in April after losing 4.64% in March. Market gain was led by the Industrial sector, which jumped 21% in the month. During April, total volume traded jumped 63% to 655 mn while total value traded increased 12% to USD 533 mn.

Bahrain

The Index was flat in April after gaining just 1% in March. Investment sector lost 5.86% for the month while Commercial Banks gained 7.89%.

In April, total value traded increased 35% to USD 37 mn while total volume decreased 27% to 65 mn. Concentration of the top five stocks in terms of volume and value to the market capitalization was 9% and 12%, respectively.

###

About Kuwait Financial Centre “Markaz”:

Kuwait Financial Centre S.A.K ‘Markaz’, with total assets under management of over KD 880 million as of December 31, 2008 was established in 1974, and has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997; and was awarded a BBB+ corporate rating by Capital Intelligence Ltd.