_36.jpg)

Kuwait Financial Centre “Markaz” recently released its Monthly Market Research report. In this report, Markaz examines and analyzes the performance of equity markets in the MENA region as well as the global equity markets.

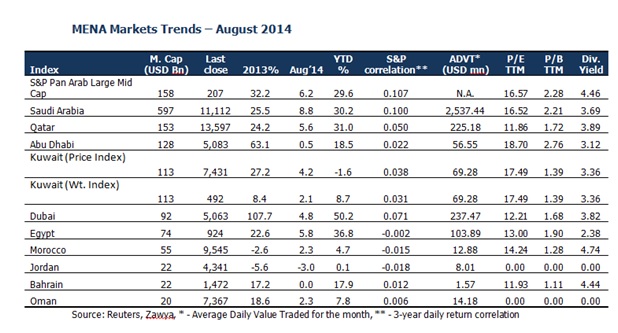

Overall, the Gulf markets had a positive month, as almost all MENA indices ended August in green. Saudi Arabia (8.8 per cent), Egypt (5.8 per cent) and Qatar (5.6 per cent) indices were the biggest gainers, while Jordan (-3 per cent), Bahrain (0 per cent) and Abu Dhabi (0.6 per cent) lagged behind. In the first half of 2014, GCC corporates posted a 11 per cent growth over the equivalent period last year, according to our recent research. Earnings were driven by strong performance in banking and financial services, telecom, conglomerate, and real estate sectors. Banks in the GCC reported double-digit profit growth, largely attributed to higher net interest income, non-interest income, and a drop in provisions, despite increase in operating expenses.

The opening up of the Tadawul exchange to foreign investors and the possibility of inclusion in the MSCI Emerging Market index in 2017 has buoyed the retail investors, who make up the majority in the exchange. Positive sentiment notwithstanding, the Saudi economy is flourishing, with strong economic fundamentals backing the market. Petrochemical companies ruled the roost, on the back of strong global demand, and with oil price remaining above the USD 100-mark.

Saudi Arabia was the biggest gainer in the first half-year earnings in the GCC, with a 20 per cent increase compared to the same period in 2013, propelled by telecom and real estate sectors. The TASI exchange has moved up by over 30 per cent since the beginning of this year, and has crossed the 11,000 mark for the first time in six years.

Egypt’s main index soared in August, as positive performance by the banking sector in the first half of the year, and investor optimism over stabilizing economy improved market sentiments. Egypt’s President Abdel-Fattah El Sisi has announced a slew of projects to revive the economy, the most recent of which was the USD 4bn Suez Canal expansion project for improving trade volumes. The contract for this project was awarded to several GCC-based companies, including a Riyadh-based planning, design, management and supervision consultancy.

Qatar index recorded a new high of 13,993 points in August, as MSCI increased the weights of three Doha-listed firms, Qatar National Bank (QNB), Industries Qatar (IQ), and Qatar Islamic Bank (QIB), in its emerging market index. This increased passive inflows, into QNB and IQ in particular, and investors buying dividend paying stocks has resulted in the surge. Although, funds tracking the MSCI frontier indices exited from both Qatar and UAE through a series of monthly sales, Qatar had a positive month on account of the above two factors.

In the early half of the month, investors in the Kuwait market had played a wait-and-watch game, as fears of ban in trading activity due to delay in disclosure of semi-annual results resulted in low trading. However, most companies disclosed their financial results before the end of the legal period, which activated purchasing of shares, especially in the small-cap segment. In terms of earnings, banking and commodities sectors had shown robust growth in the first half of 2014, gaining 18 and 52 per cent, respectively, on a YoY basis, while real estate, conglomerates and construction related sectors recorded decreases in earnings.

With the GCC markets on the uptake, S&P GCC recorded an increase of 6.4 per cent in the month of August, and closed at 148 points. Global Markets also posted positive results in August, as S&P 500 and MSCI World rose by 3.8 and 2.0 per cent, respectively, while Emerging Market rose by 2.1 per cent. S&P 500 had a record month, despite a bad start on account of geopolitical worries. Better-than-expected U.S. consumer confidence, coupled with positive earnings results and rebound of business activity helped the index breach the 2000-mark milestone.

MENA IPO markets on a rollMENA IPO market raised USD 2.4bn from 16 IPOs, in the first half of 2014, compared to 12 IPOs worth USD 2.1bn in the equivalent period in 2013. This has been the market's best performance in terms of volumes and proceeds, since the economic crisis in 2008, when it raised USD 9.4bn from 36 issues in the first half of 2008. Of the seven private equity exits in the first half of 2014, three were done through IPO route.

GCC countries had the largest share of IPO listings in MENA, constituting nearly 78 percent of capital raised from 64 IPOs between 2009 and 2014. This increased in H1, 2014, as they accounted for 90 percent of the capital raised through IPOs in MENA, with 10 IPOs raising nearly USD 2.2billion. Saudi Arabia was the prime issuer in terms of number of issues and capital raised, as the country accounted for nearly 38.5 percent of total proceeds raised from 41 IPOs between 2009 and 2014. In the first half of this year, the Kingdom accounted for four IPOs worth USD 533.3mn, including the much anticipated listings of Abdul Mohsen AlHokair Group (USD 220mn) and Al-Hammadi Company (USD 168mn).The largest deal in H1, 2014 was by Mesaieed Petrochemical Holding Company, Qatar’s first IPO since 2010, which brought in USD 0.9billion, and accounted for 38 per cent of the capital raised in the period. In the UAE, three new issues contributed to 22 percent of total capital raised in MENA.