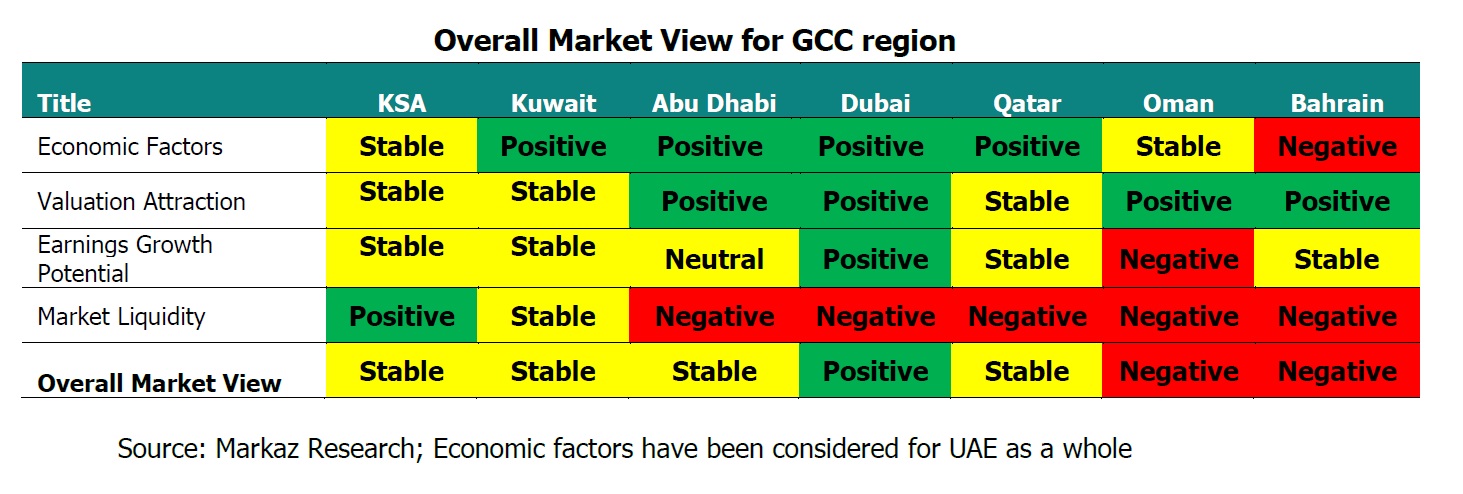

Kuwait Financial Centre “Markaz” recently released its outlook on GCC markets for the full year of 2020. In this research report, Markaz analyses the performance of GCC stock markets in 2019 and provides an outlook for 2020 based on a four-force framework that includes economic outlook, corporate earnings potential, valuation attraction, and market liquidity, for all the GCC markets.

Markaz report said that the year 2019 was characterised by average oil price at levels lesser than that of 2018, fears of global slowdown, and uncertainties over U.S–China trade war, Brexit and interest rate cuts by most Central Banks. In addition to these, weakness in real estate and commodity markets, OPEC+ production cuts, market reforms and index inclusions were the prime market drivers in GCC. At the start of 2019, we were positive on Kuwait and UAE and stable on Saudi Arabia and Qatar. Except UAE, other markets moved in line with our expectations.

The report pointed out that the oil prices in 2020 are expected to remain around 2019 levels, in the range of USD 61-65 per barrel, in spite of recent geopolitical spikes, and we expect a moderate improvement in corporate earnings. GCC governments’ expansionary spending is expected to aid non-oil economic growth, while global economic conditions also seem conducive. Given the modest oil price outlook and proposed spending plans, government finances are expected to be strained.

Kuwait – Stable

Kuwait emerged as the top performer amongst its GCC peers in 2019, with a return of 23.7%. This strong performance was mainly because of the capital market reforms, S&P index inclusion and expectation of inclusion in the MSCI Emerging Markets Index. Relaxation of foreign ownership restrictions in banks has also aided in fund inflow.

Corporate earnings have seen a moderate growth of 1.0% for the first nine months of 2019 which when compared to the same period last year is dragged down by the financial services such as investment companies, insurance firms and Non-banking financials. Banking and telecommunications have been relatively strong performers. In terms of stock return amongst blue chip companies, Kuwait Finance House (KFH) had the highest returns at 45.8%. Progress in its ongoing merger with Ahli United Bank, which is expected to increase KFH’s profit considerably and strong earnings growth, which was at 12.7% for the nine month ending September 2019, have helped it in its strong performance.

Compared to its GCC peers, Kuwait enjoys a fiscal surplus. However, we see the gap narrowing in 2020. Compulsory transfers to Future Generation Fund and subsidies seem to weigh on its balance sheet.

Saudi Arabia – Stable

The Saudi Tadawul index has gained 7.2% in 2019. Consumer services sector index gained most at 34%. Listing of Saudi Aramco has been the event of the year in the Saudi Arabian stock market. The company garnered a valuation of USD 1.71 trillion, lesser than the USD 2 trillion expected by the Saudi government. The lower valuation was against the backdrop of lower average oil price levels compared to 2018 and investor concerns over drone attacks on Saudi oil facilities. However, the stock briefly reached the sought after USD 2 trillion valuation on its second trading day.

Corporate earnings for first nine months of 2019 registered a drop of about 24.1%. Telecommunication and banks posted modest gains. Earnings growth in telecommunication has been supported by increase in volume. Strong loan growth helped the banks post profits amidst declining interest rates. Construction has bounced back after registering a dip in 2018. Commodities, Utilities and Real Estate have reported weak earnings. Weakness in the commodities sector is attributed to slower global growth and weaker oil prices. Utilities earnings have dipped because of decrease in volume. A drop in property prices hit Real Estate. In terms of stock return amongst blue chip companies, Al-Rajhi Bank had the highest returns at 14.8% whereas, SABIC witnessed a 19.4% loss in its share prices in 2019.

In Saudi Arabia, deficit has widened and is expected to widen further in 2020. Increased government spending towards Vision 2030, decrease in oil production would contribute to widening deficit in spite of an increase in revenues with the introduction of VAT and other consolidation measures.

Dubai - Positive

Dubai stock index has gained 9.3% in 2019. Banking and Insurance sector indices have performed well in the year gaining around 27% and 22% respectively on the back of better profit numbers. Hit by increasing supply, falling prices and shrinking profits, real estate sector index ended the year in negative territory, with a decline of 9.8%. Among the blue chips, Emirates NBD Bank posted an annual stock return of 52.3% supported by strong earnings over the first nine months of 2019. Earnings growth remain healthy supported by banks. Economic growth in 2020 is expected to be supported by tourism and hospitality sectors benefitting from Dubai Expo 2020. Efforts taken by the UAE government and Dubai Land Department (DLD) to stabilize real estate sector should also pay off. In terms of P/B ratio, Dubai’s (0.9x) P/B ratio is lower compared to Saudi Arabia, Kuwait, Qatar and Abu Dhabi, making it more attractive.

Abu Dhabi – Stable

Abu Dhabi index gained modestly with 3.3% in 2019. Increase in foreign ownership limits seems to have aided stock gains. Amongst blue chips, First Abu Dhabi Bank’s stock gained by 7.5% supported by increase in foreign ownership limits and good earnings growth. However, the gain had been stunted, as its representation had not been increased in the MSCI Emerging Markets Index after relaxation of its ownership limits. Commodities sector has helped boost earnings in Abu Dhabi. However, expectations of 4 per cent growth for corporate earnings in 2020 and modest valuations cap the upside potential.

Qatar – Stable

Qatar Stock Index saw modest growth of 1.23% in 2019. Top gainer for the year was Consumer Goods and Services at 26.6%. Banks and Financial Services sector gained 9.3% supported by good earnings growth. Real Estate has decreased the most with a decline of 30% with the sector experiencing falling prices and increasing supply.

Corporate profits dropped by 6.6% on for the nine-month period ending September 2019. Telecommunications posted highest earnings growth at 18%. This was driven by cost efficiency and slight increase in revenue. Industrial Conglomerates sector reported about 47% decline in earnings citing weak demand for petrochemicals and steel. Banking sector has posted a 6% growth in profits. In terms of stock return amongst blue chip companies, Mesaieed Petro had the highest returns at 65.7% whereas, Industries Qatar lost 23.1% in 2019.

Qatar is expected to see an increase in fiscal surplus in 2020, through rise in revenue from the imposition of excise duty on tobacco and increased Liquefied Natural Gas (LNG) production. Qatar exports are expected to rise once the Barzan natural gas facility comes online in 2020, helping it post a surplus in spite of lower expected energy prices.

GCC Fixed Income Outlook 2020

De-escalation of trade tensions, better growth indicators for 2020 and benign inflation would continue to provide favorable support for GCC fixed income asset class. Interest rates, that closely track U.S Fed movements, are on hold for time being and in the worst case might only rise marginally. As we step into 2020, the outlook for GCC fixed income asset class looks promising. High positive yields, better risk-adjusted returns, currencies pegged to US Dollar and improving credit quality on the back of rising oil prices augur well for their improving stance. On the other hand, increasing oil prices could lead to a sense of complacency on the reforms front. Prudent fiscal management measures for Oman and Bahrain are to be watched carefully.

We also highlighted some key questions to ponder upon as we move into 2020. We looked into the reasons behind the double-digit growth in almost all the global asset classes in 2019, despite there being a slowdown in global economic growth, trade war escalation, geopolitical risks and predictions of a likely recession. We contemplate how far Central Banks around the world can go before monetary policy becomes ineffective and whether the ever-increasing technological upgradation is actually boosting productivity. We bring to light the cries of environmentalists who have been sounding alarm bells pertaining to climate related issues and the subsequent push for clean energy and Electric Vehicles and its impact on global oil demand. Finally, we to try to answer the question of whether the global economy is truly in late cycle.