_36.jpg)

In an unprecedented decision, on the 5th of August 2011 the S&P ratings agency downgraded the U.S.'s AAA credit rating for the first time, criticizing lawmakers for failing to cut spending enough to reduce record budget deficits. The historic move signals a blow to the world’s largest economy and throws doubt on an already tentative global economic recovery.

According to a new report by Kuwait Financial Centre “Markaz”, the downgrade has wide-ranging implications, but is certainly not a repeat of 2008. Regardless of the debate, direct and collateral damage for the GCC must be assessed. The impact is not uniform as some GCC countries have more at stake on certain issues than others.

GCC Equity Markets-Post AAA Downgrade

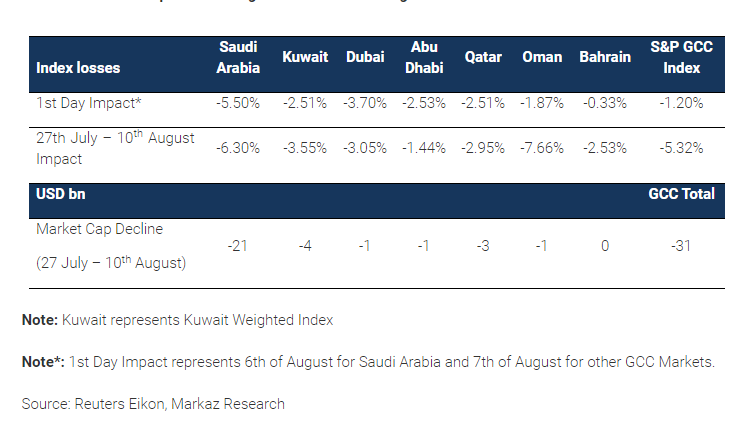

The short term effect has been felt already with GCC stock markets experiencing large declines following the announcement; Saudi tumbled 5.5% on the 6th of August. When other GCC markets opened on Sunday, they also experienced sharp declines. GCC stock markets shed USD 31 bn in market cap from the announcement of the US debt deal at the end of July to the downgrade. The stock markets could decline further as international markets fluctuate wildly on varying risk assessments.

Table: Immediate Impact of Downgrade on Local Exchanges

Oil: While the downgrade has triggered a fear of global double dip recession, it has not yet triggered an oil price collapse. In fact, oil prices have strengthened based on supply concerns. Even in a scenario of low prices due to a double dip recession, the Kingdom sits on a pile of reserves that can see it through its spending program. Saudi Arabia requires a breakeven oil price of $72/barrel to balance its budget at current levels and the Institute of International Finance (IIF) anticipates another 15 years before breakeven oil prices hit $110/bbl. Hence, risks triggered by rating downgrade resulting in oil price crash is misplaced at least for the short term.

Domestic Investments: Saudi Arabia has been on a strong investment drive over the last few years and this is expected to continue irrespective of global events. Motivation behind such investments (for e.g., employment) is too strategic to sway year on year based on global developments. Continuation of such domestic investment program in light of strong liquidity is a strong possibility.

Stock Market: The stock market has already reacted to the US downgrade; the TASI is down 7.5% for the year. Furthermore, if cost of equity goes on the rise, it would have a declining effect on company valuations which may cause a sell-off as brokers decrease their Fair Value assessment of firms.

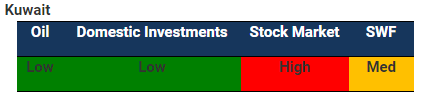

Oil: Like Saudi Arabia, Kuwait has built considerable reserves during the oil boom. It has a much larger store of reserves (on a GDP/capita basis) as budget expenditure grew more moderately during the last few years when benchmarked with Saudi Arabia. At a breakeven oil price of $70/bbl the current oil price provides a cushion of $50/bbl. Even in a scenario where oil price reaches breakeven level, Kuwait can begin to draw on its reserve pile for a long time before it drains out.

Domestic Investments: Kuwait’s domestic investments have been lagging for some time. The country’s Development Plan came in to sort out this problem; much of the USD 125 bn plan is built on government spending coupled with increasing Foreign Investor involvement. While the cost of finance is expected to rise, it may not reach a point where the domestic investments could be scaled down.

Stock Market: The stock market has already declined 15% for the year and has become hypersensitive to global cues; consequently, sustained negative news (such as a worsening of the Euro-crisis, a further downgrade of the US or a downgrade of another G7 nation) would cause further declines to the market.

SWF: The sovereign wealth fund, Kuwait Investment Authority (KIA), receives the majority of the government’s revenues for investment purposes; and the same is deployed on a globally spread portfolio across various asset classes. To the extent the SWF investments are exposed to US treasuries and the US$ currency, it runs the risk of value erosion. However, the authors don’t foresee a significant decline in KIA’s earnings as investments tend to be geographically spread rather than concentrated in one country or risk-bracket.

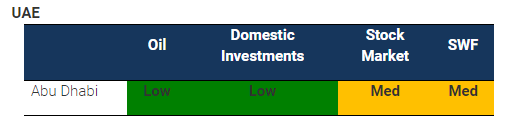

Given that much of Abu Dhabi’s economic growth and diversification strategy is dependent on government spending of oil revenues, a prolonged decline in oil prices could put a damper on progress. However, the report indicates that given the reserves built up in addition to the wealth generated and deployed by the Abu Dhabi Investment Authority (whose assets are reportedly upwards of USD 630 bn), the emirate should be able to maintain its spending plans despite any nominal decline in the value of its reserve assets.

The Abu Dhabi stock market has remained relatively well isolated from negative global market cues; it remains one of the best performers in the GCC on a year to date basis (-5%).

Dubai is in a slightly more precarious situation given the declines suffered as a result of the global credit crisis, which it is still recovering from, in addition to the fact that it has more of a global linkage than Abu Dhabi.

Given that the Dubai economy is reliant mainly on Trade and Tourism for GDP growth, these may see a decline should world economic growth decline. Should economic growth in Dubai be hindered, it could prove detrimental to domestic investment by the government and private sector. This may also affect the confidence factor for foreign investors, who would increase their risk premium on Dubai. A further downgrade in the US and/or another G7 nation could result in cost increases for foreign and local firms.

Banks could see an escalation of risky assets as ratings change leading to a squeeze on capital adequacy ratios, which coupled with an increase in provisions would dent bottom line performance going forward. Additionally, the stock market has been performing poorly for the year, down by about 11%, and is expected to continue to be hypersensitive to global and regional cues.

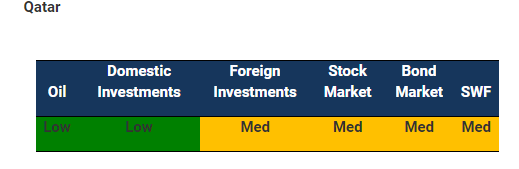

Qatar enjoys similar comfort as that of Saudi Arabia, Kuwait, and Abu Dhabi when viewed from oil and gas resources and reserves. Hence, the authors perceive lower risk on that account. Qatar has also been one of the best performing markets in the GCC over the last two years, successfully skirting the global financial crisis while maintaining its growth trajectory. Consequently, a mid-level risk is expected in terms of the stock market, which is down about 3% for the year.

The reserves and revenues built up by the State through the years would to allow it to continue to implement large-scale development plans such as the USD 125 bn National Development Strategy which was put in place this year.

Furthermore, Qatar is currently implementing many regulatory reforms and developments, such as encouraging firms to lower Foreign Ownership Limits (in order to be upgraded to MSCI Emerging Market status) in addition to setting up an organized bond market. These measures, coupled with large-scale projects relating to the World Cup 2022 event, should keep foreign investor interest sustained.

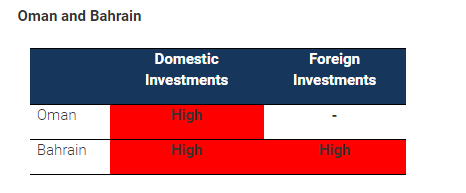

Oman and Bahrain both had a relatively difficult 1H11 with political turmoil dampening the economy and market sentiment. Oman, down 15%, is the worst performing GCC for the year while Bahrain, down 12%, is only marginally better.

Lower global growth and dampened oil demand would make it relatively more difficult for Oman to enact domestic investment programs. This difficulty is compounded by the lingering political issues, mainly relating to unemployment, which the government must address.

The impact in Bahrain is expected to be higher; the country does not have oil revenues to fall back on (the economy depends on tourism and the financial sector) in order to boost public spending and consequently, any further strain on the economy will lead to declining domestic investments. Moreover, the government currently runs a deficit of about -6% of GDP, placing further strain on government spending.

# End #

###

About Kuwait Financial Centre “Markaz”

Kuwait Financial Centre S.A.K. 'Markaz', established in 1974 with total assets under management of over KD 906 million as of June 30th, 2011, is the leading and award winning asset management and investment banking institution in the Arabian Gulf Region. Markaz is listed on the Kuwait Stock Exchange (KSE) since 1997 under ticker Markaz.