_36.jpg)

In its new research on the GCC Port sector, Kuwait Financial Center “Markaz” notes that GCC governments have benefited from high oil prices during the last several years, aiding them in reducing external debt and increasing expenditure. The majority of this expenditure has been focused on infrastructure building. Among the various facets of infrastructure development, the sea ports segment is witnessing a robust growth in investments.

The large volume of export of hydrocarbons by sea has ensured the development of ports in all Gulf countries. The GCC region’s total trade (Imports + Exports) witnessed a CAGR growth of 15% between 1994-2009E. Of this, imports from 30% and exports from the rest. Within exports, the hydrocarbon related exports constitute 90%. Also, there has been a shift in the concentration of the top three trading partners since 1994. The GCC exported 61% of its total exports to EU, Japan and US in 1994. This rate is expected to decline to 44% in 2009. This trend is similar for imports too. GCC imported 69% of its total imports from EU, Japan and US in 1994. This has declined to 53% currently.

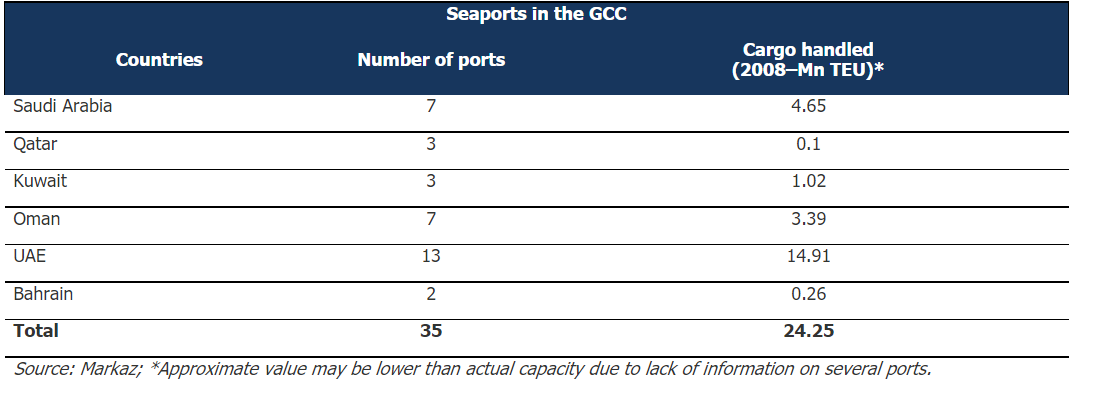

GCC seaports have witnessed robust growth rates in volume. At an overall level, the sea ports in GCC have witnessed an estimated 12% CAGR in volumes to 24 Mn TEU’s in 2008 from 15 Mn TEU’s in 2004. The UAE ports have the highest share of volume among the GCC countries at 61%. The ports in UAE have been witnessing a 13% CAGR growth in volume between 2004 – 2008. The highest growth according to our estimates is in Kuwait with a CAGR of 15%, but with a low share of overall GCC volume at just 4%.

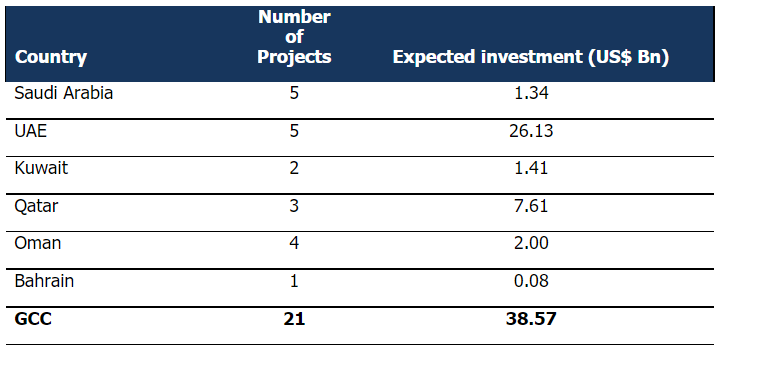

GCC countries have 35 ports in all, some of which are currently undergoing expansion to meet increasing trade demand. Total investments in GCC port projects till 2008 have touched almost US$38.2 bn, with maximum investment in the UAE (around US$23 bn). Between Jan 2008 – Jul 2009 alone, the total value of projects that have witnessed completion has been at USD 843 Mn.

Seaports in the GCC

The total value of upcoming projects is at USD 38.57 Bn. However, there are two major challenges for the ports sector in GCC. Depressed oil revenues over a long period of time might result in cancellations of some of the large port projects currently being undertaken in the GCC. Also, continuation of the financial crisis in the Middle East would result in cancellation of the projects. Our estimates show that already USD 1.68 Bn worth of projects have either been put on hold or cancelled.

Planned Seaport Projects in the GCC

GCC ports ranking

Also, some of the ports in GCC rank favorably among global peers. The Dubai port in UAE ranks the seventh among 528 ports in the world. The Dubai port handled 11 Mn TEU’s in 2008. The Dubai port has also been witnessing a high growth rate of 16% CAGR between 2004-2008. The Jeddah port in Saudi Arabia ranks 33rd among global ports with an annual throughput of 3.3 Mn TEU’s. However, the growth in throughput has been significantly lower than that of Dubai at 8%. The highest growth in throughput comes in from the Jubail sea port in Saudi Arabia at 51% but with significantly low volume and a lower base.

The GCC has in total five ports which are ranked below the 100 mark.

-Ends-Kuwait Financial Centre S.A.K. "Markaz", with total assets under management of over KD 900 million (USD 3.1 Billion) as of June 30, 2009, was established in 1974 has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. "Markaz" was listed on the Kuwait Stock Exchange (KSE) in 1997.