_36.jpg)

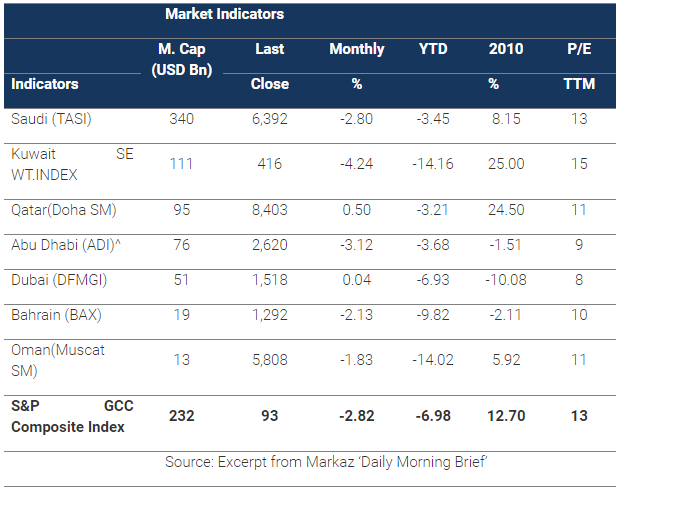

GCC markets were down again in July as investors turned their eyes to the US debt crisis in addition to on-going sovereign issues in Europe. Corporate and regulatory issues at home kept investors shying away from the market ahead of the Holy month of Ramadan. The S&P GCC lost 2.8% after shedding 2% in June, bringing YTD losses to almost 7%. Dubai was flat while Qatar eked out a gain of 0.50%. The largest decline was in Kuwait’s Weighted Index, down 4.24%.

News in the region included:

- The UAE made a surprise announcement post the conclusion of the US debt deal; the Central Bank said it had no US Treasury Bills in its reserves or any other financial instrument issued by the US government, citing “very low return”. The announcement came as a surprise given the currency peg to the Dollar. Anecdotal evidence suggests that the Central Bank has turned to Japan for Dollar-denominated government debt.

- The Kuwait market hit a 7 year low in the middle of the month, dipping below 6,000 points on a compendium on poor news. The Central Bank governor announced that the economy suffered from precarious imbalances which needed to be addressed urgently.

- The Kuwait Capital Market Authority extended the deadline for Fund compliance with investment limits, under Article 347, to March 2012 from the previous September 2011 deadline citing adverse market conditions and a need to review the article.

- Kuwait Airways privatization process has begun with a 35% stake on offer for expression of interest through August. The airlines is hoping for interest from regional or international strategic partners and will exclude local airlines.

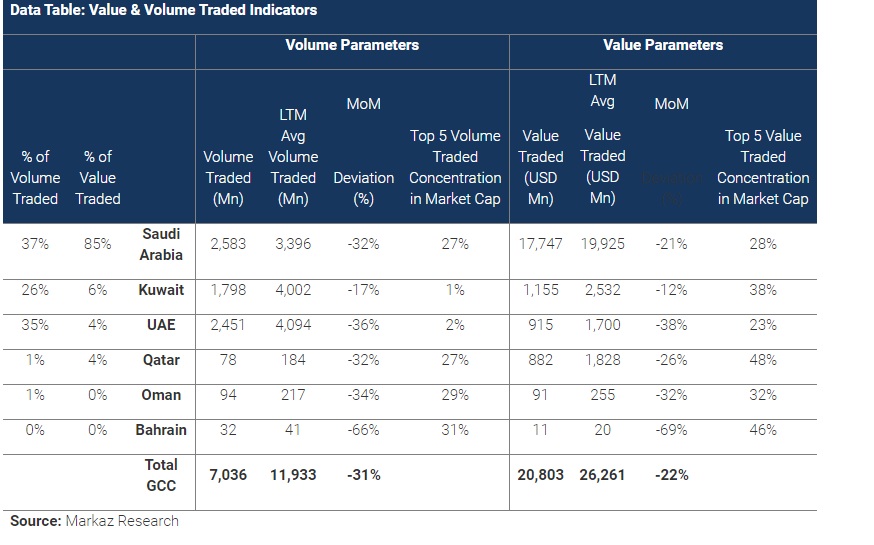

Liquidity was down significantly in July; GCC value traded declined 22% to USD 20.8 bn while volume was down 31% to just 7 bn. Saudi and Kuwait saw value traded decline by 21% and 12%, respectively. GCC Value Traded in the YTD period is at USD 215 bn, 10% higher than the same period last year.

Risk in the GCC (as measured by the Markaz Volatility Index – MVX) was up just 1% in July after increasing 21% in June. MVX Kuwait was up the most, jumping 56% for the month while MVX Qatar saw a fourth consecutive month of declines, down 37% for the month.

Global Markets review

Monthly returns were negative across the board; excepting a flat Asia Pac ex. Japan and a scant 0.17% monthly gain on the Nikkei 225. Losses were led by India and MSCI Europe which lost 3.4% and 3.3%, respectively. The S&P 500 shed 2% for the month as the debt crisis peaked.

Global markets were preoccupied with the US Debt deal saga which reached a fever pitch during the month. Gold was up on the uncertainty, gaining 8.5% for the month. Crude oil gained almost 4% for the month, with a YTD gain of almost 27%.

Investors shifted to the US as the debt crisis boiled over with political stalemates causing S&P ratings to indicate a 50% chance that it would downgrade the US if a deal was not reached as the country rapidly approached the $14.3 trillion debt ceiling. An 11th hour deal was finally struck which advocated a $2.1 trillion, 10-yr deficit-reduction plan, about half the aimed for $4 trillion. Following the announced, Moody’s affirmed the US ‘AAA’ rating but placed the country on “Negative” outlook due to low economic growth and fiscal weakness while S&P downgraded the US credit rating from AAA to AA+ with a “Negative” Outlook.

The ECB is expected to put a stop to its tightening policy as economic growth shows signs of weakening while trouble brews in Spain and Italy in addition to resuming purchases of distressed government debt.

# End #

About Kuwait Financial Centre “Markaz”

Kuwait Financial Centre 'Markaz', with total assets under management of over KD 960 million as of March 31st, 2011, was established in 1974 has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997