_36.jpg)

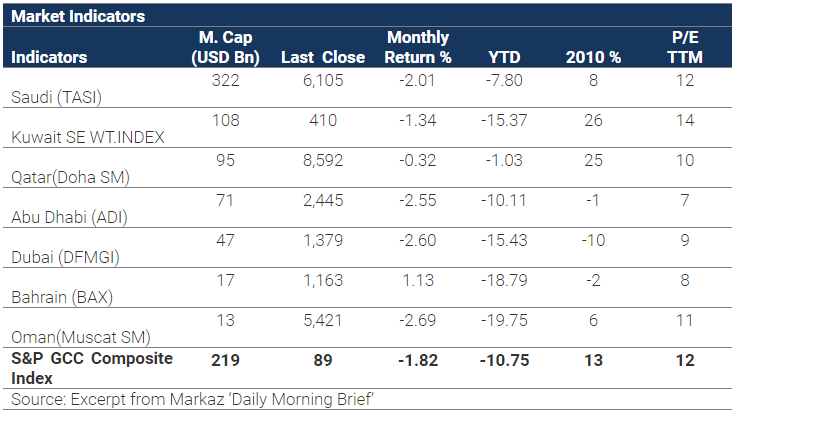

GCC markets reversed October’s gains and shed 1.82% in November (S&P GCC Composite) as political unrest flared up once more. The largest declines were in Oman (-2.69%) and Dubai (-2.6) while Bahrain managed a gain of 1.13%.

News in the region included:

- MSCI is expected to release the results of its market classification review on the Qatar and UAE markets by the middle of December. MSCI delayed the results, which were initially expected in June, as Qatar and UAE were implementing measures to enhance their markets such as adopting new trading technology in addition to FIF limits.

- Saudi Arabia Money Supply grew 14.4% YoY in October versus 12% in September. Lending to the private sector grew 10% YoY in the same month and is expected to accelerate in 2012.

- The UAE set up a $2.7bn fund to pay down debt for some low-income citizens; moreover, the country with be doubling wages for state employees beginning January 2012.

- Kuwait Inflation rose to 4.8% in October (up from 4.5% in September) due to a rise in global commodity prices in addition to monetary appeasement measures by the government. In October, the governor of the Central Bank expressed concerns regarding the debt issues in the Euro-area and stated that current interest rate settings were appropriate.

- Qatar successfully sold a $5bn, three tranche bond (5-yr, 10-yr, and 30-yr maturities) with orders amounting to $9.5bn. The bond is expected to be used in financing Qatar’s development and infrastructure spending over the coming years.

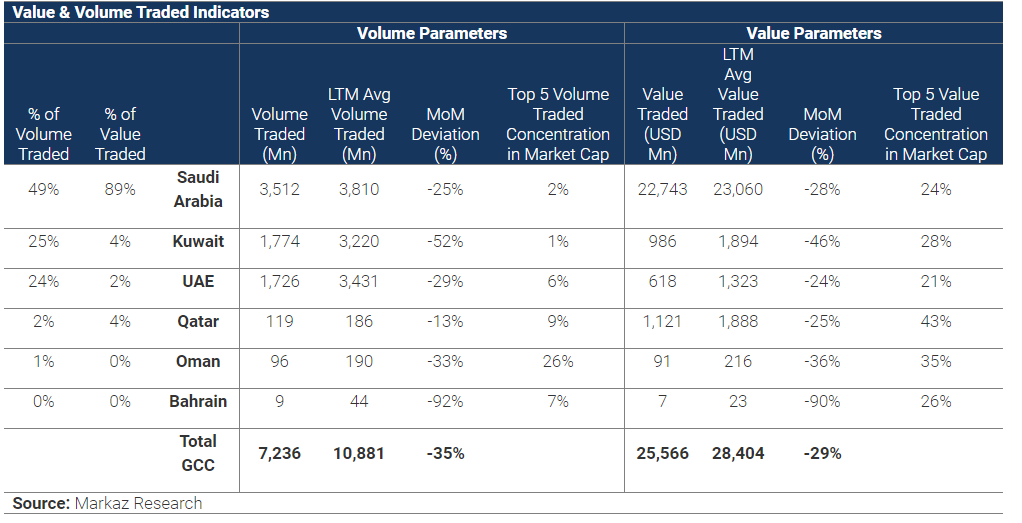

Liquidity was down 29% in November after a strong showing in October. All markets saw double digit declines in trading. GCC value traded was at $25.5bn while volume was down 35% to 7.2bn. GCC Value Traded in the YTD period is at USD 316bn.

Risk in the GCC (as measured by the Markaz Volatility Index – MVX) declined 2% in November after shedding 19% in October. The decline was mitigated by Kuwait where risk was up 19% during the month while MVX Bahrain was up 33%.

Global Markets review

Monthly returns were positive across the board. After a 14% drop in September, Asia ex. Japan came back strongly gaining 13% in October. Europe gained 12% and S&P gained 10.8%. Frontier markets registered the lowest gain of 2.1%

World markets surrendered some of the high gains made in October as equities slumped amid a rising concern that the Euro may be heading for dissolution. Gold and Crude Oil were flat for the month after logging gains of 7% and 4%, respectively, in the previous month.

As concerns over a pending Euro dissolution reached a fever pitch towards the end of the month, Eurozone officials eagerly sought to calm markets and investors by seeking a more comprehensive solution to the continent’s sovereign debt problems. Coordinated monetary easing measures by major central banks in response to signs that a new bank funding problem is emerging led to short rally at the end of the month, but most markets still ended in negative territory.

The broad World Index shed 2.9% in November bringing the YTD loss to 6.7%.

# End #

###

About Markaz

Kuwait Financial Centre 'Markaz', with total assets under management of over KD906 million as of June 30, 2011, was established in 1974 has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997.