_36.jpg)

The S&P GCC managed to eke out a gain of 0.36% in September after tumbling 5.12% in August. However, the majority of indices still had a highly negative month, led by a 7.35% decline in Bahrain amid renewed political tensions. The S&P GCC index was bolstered by a 2.23% gain in Saudi while Kuwait’s weighted index was up 1.56%.

News in the region included:

- A report by SAMA indicated that the kingdom’s banks were well-capitalized and protected against shocks to the system. Over the past two years, the banks have undergone a high degree of provisioning, bringing coverage of NPLs to 118%, according to the head of the central bank.

- According to the Ministry of Finance, Kuwait needs a breakeven oil price of $75/bbl for the current budget. A KD 6 bn deficit has been budgeted for the fiscal year 2011/2012, but given the high oil prices during the year, this will be another surplus year for the country. The first quarter of the fiscal year showed a surplus of almost KD6bn (USD 20bn). The ministry went on to say that while they were monitoring the situation in the Eurozone, more substantial exposure was in the US.

- The proposed $950mn sale of Zain’s 25% stake in Zain Saudi has been scrapped. The consortium of Batelco and Kingdom Holding walked away from the non-binding offer which was made earlier in the year, noting that terms of the deal could not be met.

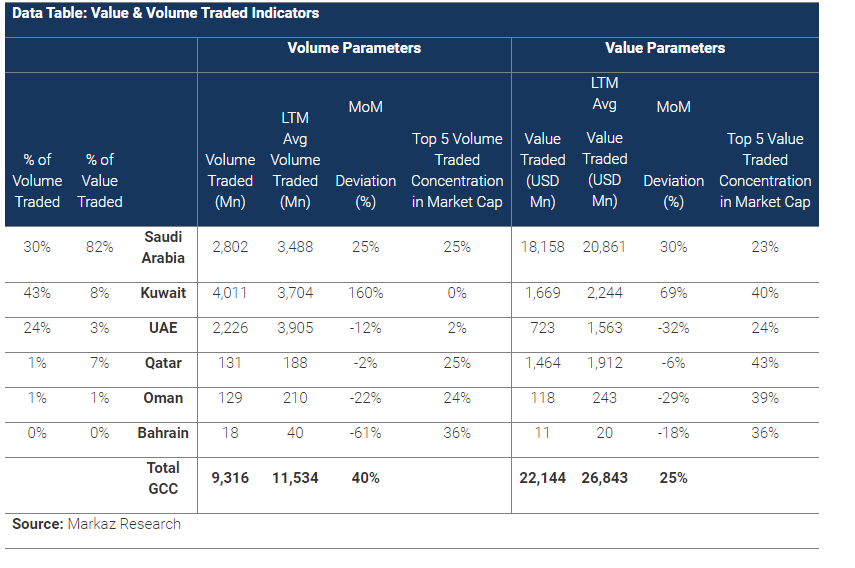

Liquidity was up in September due to strong trading in Saudi Arabia and Kuwait, where value traded was up 30% and 69%, respectively. GCC value traded increased 25% to USD 22 bn while volume was up 40% to 11.5 bn. GCC Value Traded in the YTD period is at USD 254 bn. On a quarterly basis though, value traded was down by 41% across the GCC led by a 42% drop in Saudi Arabia value traded for 3Q11.

Risk in the GCC (as measured by the Markaz Volatility Index – MVX) was down 17% in September after jumping 28% in August, with the Q3 change coming in at 7%. The highest monthly jump was in MVX Bahrain, whose MVX more than tripled on account of renewed political tension. On a quarterly basis, MVX Dubai saw the highest decline of 44% while MVX Kuwait was up 34%.

Global Markets review

Monthly returns were highly negative across the board; the worst performance came from Asia ex. Japan, falling nearly 14% followed by MSCI Europe down nearly 12% for the month after declining 10.4% in August. The least losses were in India (-1.3%) and Japan (-2.8%).World markets saw even steeper declines in September as the Eurozone debt crisis intensified, with a Greek default seemingly imminent. Investors remain concerned that the crisis could have severe global implications on an already weakening economic recovery. Markets have become hypersensitive to European cues; the S&P500 shed 13% in 3Q11, the worst decline since the last quarter of 2008. More than USD 10 trillion was wiped from world markets during the third quarter of the year while VIX shot up 160%.

The broad World index tumbled by 9.4% for the month bringing the YTD loss to 13%.

# End #

###

About Kuwait Financial Centre “Markaz”

Kuwait Financial Centre S.A.K. 'Markaz', established in 1974 with total assets under management of over KD 906 million as of June 30th, 2011, is the leading and award winning asset management and investment banking institution in the Arabian Gulf Region. Markaz is listed on the Kuwait Stock Exchange (KSE) since 1997 under ticker Markaz.