_36.jpg)

In its recently released research note has examined the opportunities for distressed real estate investment in the GCC region. As against the popular understanding of distressed investment, which involves buying real estate asset or property at distressed pricing from a seller who is either distressed or otherwise, the report intends to identify attractive markets which are priced at distressed levels. The authors have conducted a market level assessment of both residential and office space in order to ascertain the attractive market for distressed investment.

The authors opine that the real estate prices remain depressed amidst a macroeconomic scenario which is increasingly stabilizing. Obtaining credit continues to remain a tough task. The combination of these conditions could be a pool of distressed investment opportunity for investors. They have analyzed the current scenario in the GCC real estate market in a systematic way to identify the land of distressed investment opportunity.

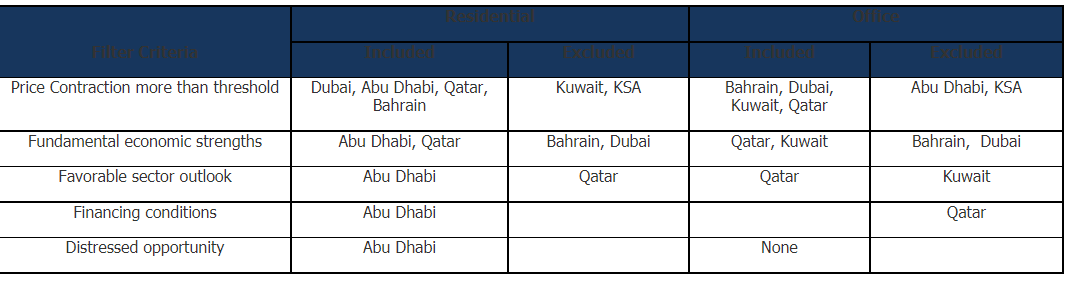

In order to adjudge a market to have priced at “distressed” levels, it is necessary that the prices should have contracted to a considerable extent. A significant price correction indicates that the market is priced at distressed levels, however, for it to be adjudged “attractive”, they should have a promising future prospects. The attractive distressed market should also be providing with opportunities to tap. A market which is adequately funded would not provide with many distressed opportunities to tap and hence would not be ideal place to look for investment. Hence, a market which is besieged by financing troubles, where prices have contracted considerably and where the future prospects are brighter, should be the best market to look for investment opportunities.

Price contraction : The authors compared the price contraction in both residential and office space in each GCC market with that of a threshold contraction. The threshold was determined as 26% for residential and 32% for office space after studying the price contraction in 42 markets across the world with a 3-5% additional inclusion range in order to avoid exclusion due to marginal differences. Prices of residential real estate in Dubai (-47%), Abu Dhabi (-47%), Qatar (-26%) and Bahrain (-24%) contracted more than the threshold and prices of office space in Bahrain (57%), Dubai (48%), Kuwait (43%) and Qatar (27%)contracted more than threshold and passed the filter for price contraction. Residential markets in KSA and Kuwait and Office sector in Abu Dhabi and KSA got excluded, as they have not fallen beyond the threshold as yet.

Economic Fundamental Strength : In order to avoid getting the investment locked up for a prolonged period, the authors looked at the fundamental strength of each economy, using two criteria, the ability of the economy to bounce back quicker and better from the current slump and the economy’s exposure to the troubled real estate and financial services sector. Abu Dhabi, Kuwait and Qatar fared better in the bounce back expectations while the expectations were poor in case of Dubai and Bahrain. In much the same way, Dubai and Bahrain had a higher exposure to the troubled sectors at 26% and 23%, compared to Kuwait (16%), Qatar (10%) and Abu Dhabi (9%). Thus, Dubai and Bahrain got filtered out due to poor economic strength.

Real Estate Sector Outlook: In order to recover along with the economy, the sector should not suffer from current and short term oversupply. Current oversupply can be measured from rental contractions and Abu Dhabi (residential) contracted only by 1% which is indicative of its strength while Qatar contracted by 27%, indicating oversupply conditions. Office rentals contracted heavily in both Qatar and Kuwait, however, since demand for office space is more sensitive to economic growth, it would bounce back once the economic recovery is in place. In order to estimate the short term oversupply, the authors looked at the short term supply pipeline. 29% of total office projects is expected to be completed before 2010, compared to 8% in Qatar. Hence, Kuwait office gets excluded while Qatar office can be considered for distressed investment.

Financing conditions : Contraction in banks’ asset size and increased capital requirements with expected losses from RE loans should lead to lower willingness and ability to RE lending in UAE thus providing distressed investment opportunity while banks in Qatar is in a good position to lend viable projects thus forbidding any distressed investment opportunity.

Opportunities and Risks in Abu Dhabi (Residential) : Development statistics indicate that close to 35% of the value of all residential developments are under construction and only 10% of them are in initiation stage and the rest are in planning stage. Anecdotal evidence suggests that the sub-developers of master developments are facing troubles in getting financing, thus providing with avenues for distressed investment. The locational proximity to the oversupplied Dubai could act as a drag and tough credit conditions may prolong price recovery.

###

About Kuwait Financial Centre “Markaz”

Kuwait Financial Centre S.A.K. "Markaz", with total assets under management of over KD 900 million (USD 3.1 Billion) as of June 30, 2009, was established in 1974 has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. "Markaz" was listed on the Kuwait Stock Exchange (KSE) in 1997.