_36.jpg)

Kuwait Financial Centre “Markaz” recently released a semi-annual review of its “What to expect in 2011” report in which the authors discussed the myriad triggers which negatively impacted the GCC markets in 1H11 and how they altered Markaz outlook on the markets for the remainder of 2011.

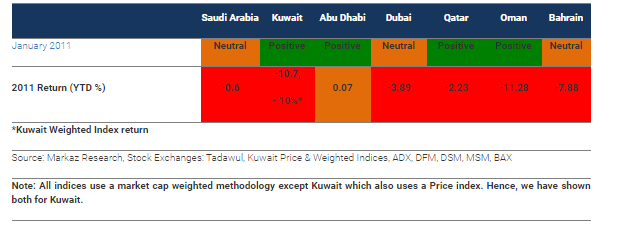

In Markaz’s previous note, the authors had upgraded their outlook to a mostly Positive view on the region. This was due to many factors including; healthy economic growth, expected recovery in key sectors like Banking and Real Estate in addition to healthy valuations. The report had a Neutral stance on Dubai (due to persisting debt overhang and a struggling Real Estate sector), Bahrain (due to lesser corporate recovery), and Saudi Arabia (due to muted banking performance and investor sentiment).

Since then, the political turmoil which swept the region at the beginning of the year brought down all markets and proved a drag on earnings. Additionally, various corporate issues (in terms of M&A, debt restructuring etc) in addition to some regulatory and market developments (Kuwait CMA, MSCI not upgrading of UAE and Qatari markets etc) has dampened investor sentiment across the board.

Previous Recommendations & Market performance

For the rest of 2011, the report has adopted a rather Neutral view of the markets due mainly to muted earnings growth and lackluster market liquidity and activity. The authors remain Positive on Abu Dhabi and Qatar due to positive economic growth and earnings potential.

Country Views

Saudi Arabia – Neutral

The report maintains a Neutral outlook on Saudi Arabia for 2H11 due to moderate economic activity (especially inflation and the fiscal balance) in addition to moderate earnings growth. Positive factors arise in valuation and market liquidity which has been picking up.

The 2011 Saudi fiscal budget is expected to run a deficit of USD 10 bn, with spending forecasted at USD 154.7 bn (7% lower than actual 2010 expenditures of USD 167 bn). The budget is expected to show increased infrastructure spending. The Kingdom’s $385 bn, 5 yr development plan is expected to spur economic activity by encouraging construction/real estate projects, which in turn should spur lending by banks. The program includes housing, ports, and upgrading the educational system.

Additionally, the government has ramped up spending on welfare programs and Saudization plans in order to quell civil unrest and address its unemployment issues. Consequently, the fiscal balance is expected to drop from 13% of GDP in 2011 to 9% in 2012.

As for corporate earnings, these are expected to be flat in 2011 versus a 30% growth in 2010 (which was largely driven by Commodities). Support is expected to come from the Banking sector, which are estimated to grow at 10% in 2011 while slower growth in telecoms may be a drag on overall earnings. Investor sentiment (as measured by Bayt.com) was up 13% as of March 2011 while the geopolitical outlook (as measured by EIU) remains stable despite some signs of unrest at the beginning of the year.

As previously mentioned, market liquidity is up in the Kingdom. Value Traded came in at USD 155 bn for 1H11, a 28% YoY growth, which would translate to over USD 300 bn if the pace keeps up to the end of the year.

Kuwait – Neutral

The authors have downgraded the outlook on Kuwait from Positive to Neutral for the remainder of 2011 due to poor market conditions, more muted earnings growth and continued weakness in market liquidity.

The economy is expected to grow by 5.3% in 2011 following a growth of 2.3% in the previous year, aided by high oil prices and increased government spending. This growth is expected to be maintained through 2012. Inflation, which is expected to have jumped to 6.1% in 2011, due to subsidies and grants, is forecasted to come back down to 2.7% in 2012. This is below the long-term average of about 4%.

Fiscal and Current Balances are expected to remain the highest in the Gulf, at 23% and 37% of GDP, respectively, in 2011 and holding steady through 2012.

Corporate earnings in Q1 were fairly positive; aggregate net profit was at USD 2.14 bn, boosted by extraordinary telecom earnings and a return to positive results for the financial sector. However, full year 2011 results are expected to come in at USD 5.6 bn, a 3% decline from last year.

UAE – Abu Dhabi: Positive, Dubai: Neutral

The authors remain Positive on Abu Dhabi while being Neutral on Dubai. The economy grew at an estimated 2.4% in 2010 and is expected to show a growth of 3.3% in 2011 followed by 3.8% in 2012. Inflation is expected to jump to 4.5% in 2011 versus 2% in 2010. The geopolitical and regulatory arenas are considered to be stable. However, lack of liquidity remains a problem as value traded in the UAE continues to dry up.

Corporate earnings are expected to rebound in 2011 after the Real Estate sector suffered a significant loss in 2010 (due to Aldar Properties). 1Q11 was a little weak, aggregate net profit was at USD 2.8bn, a 1% decline. However, a return to profitability in the Real Estate segment should push aggregate net earnings in 2011 to USD 10.2 bn. Banks are expected to show a net profit of USD 5.36bn, a 17% annual growth.

Qatar – Positive

The authors remain Positive on Qatar owing to its high economic growth prospects, healthy banking sector and heavy government support in addition to increasing liquidity. The economy is expected to show another year of double-digit growth, boosted to a forecasted 20% in 2011 (due to high commodity prices) before falling back to a more sustainable 7% in 2012.

1Q11 net profits came out to USD 2.4bn, a 23% YoY growth. Corporate earnings are expected to continue growing at a healthy pace to USD 8.5bn by the end of the year, which would translate to an annual growth of 12%.

Bucking the GCC trend; Qatar value traded grew in 1H11 to USD 12.95bn, a 33% YoY growth. Should the government be successful in raising Foreign Ownership Limits (a prerequisite for MSCI Emerging Market inclusion), liquidity could increase significantly in the coming year.

Oman – Neutral

The outlook on Oman has been downgraded from Positive to Neutral due to the political situation which impacted corporate earnings, sentiment and geopolitical perception.

Real GDP is expected to have grown at 4.7% in 2010 to decline to 4.4% in 2011 and down to about 4% in 2012 as economic growth slows. Consequently, inflation is also expected to decline through the years; it is forecasted at 3.5% in 2011 before declining to 3% in 2012.

Corporate earnings in Oman were impacted by the political turmoil at the beginning of the year, coming in at USD 338 mn, a 26% YoY decline. Some weakness is expected to remain throughout the year, specifically in the financial services and Telecom sectors, with full year net earnings at USD 1.5 bn, a 5% annual decline.

Bahrain – Neutral

The report gives a Neutral outlook on Bahrain, but verging on Negative due to weakened corporate earnings outlook in addition to a less than favorable geopolitical environment which is negatively impacting investor sentiment and market liquidity.

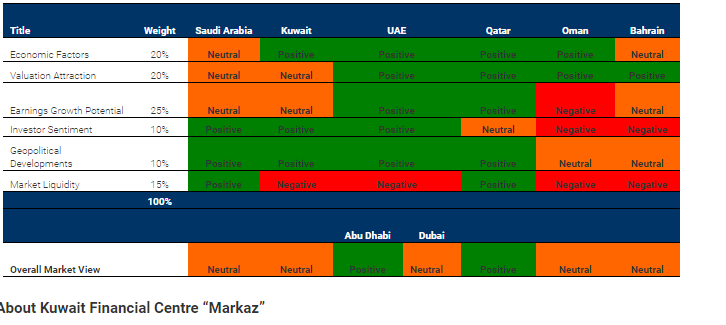

The report provides an outlook for 2011 by using the six forces framework which includes 1. Economic Factors, 2. Valuation Attraction, 3. Earnings Growth Potential, 4. Investor Sentiment, 5. Geopolitical Developments, 6. Market Liquidity.

Economic Factors: GDP Growth: Real GDP across the GCC is likely to show a growth of about 5% in 2011 followed by a growth of between 5%-7% in 2012. Growth in 2011 has been driven by spiking crude oil prices at the beginning of the year coupled with some return in private credit and broad money growth in addition to increased government spending. Growth in Saudi Arabia is expected to show a surge of 7.5% in 2011 due to high oil revenues, however, this is expected to fall to about 3% in 2012. Kuwait GDP growth is expected to remain stable at about 5% for 2011/2012. Qatar, which has had the world’s highest growth rates over the last few years is expected to show another year of double digit growth at 20% for 2011 before dropping to the more sustainable 7% in 2012.

Inflation: Both Saudi Arabia and Kuwait saw jumps in inflation during 2011 due to government grants and subsidies; according to the IMF, CPI is expected to show an increase of 6% for each country in 2011. This should moderate in 2012 as economic growth slows; coming in at 5.6% for Saudi Arabia and 3% for Kuwait.

Fiscal Deficits: Fiscal balances are expected to show a jump in 2011 due to high oil prices at the beginning of the year (crude oil was up about 25% in the first quarter) which boosted coffers before declining in 2012 as governments engage in increased public spending as per development plans.

Current Account Balance: According to the IIF, the consolidated current account balance of the GCC is estimated to reach over $150 bn in 2011 (from $124 bn in 2010) on account of a positive commodities environment.

Broad Money Growth: Money supply growth remained sorely below average in 2010, except in the case of Qatar which saw M2 grow at 23% for the year while other GCC countries saw growth as low as 3% (Kuwait) to 11% (Oman and Bahrain).

Valuation Attraction: Normalizing earnings growth coupled with poor market performance is stretching valuations in some cases. GCC corporate earnings came in at USD 13.78 bn in 1Q11, a 19% YoY growth. The highest growth is expected from the UAE, recovering from losses sustained in the Real Estate sector in 2010. Full year net profit is expected at around USD 48 bn, a 15% annual growth.

Consequently, the GCC-wide PE should stay in the 14x-15x range, on par with 14x for MSCI EM and 15x for the S&P 500.

Earnings growth potential: At the beginning of the year, the authors were quite positive on all countries in terms of earnings growth due to several rebound stories. However, despite a more or less positive Q1; the report gives a Neutral view on Saudi Arabia, Kuwait and Bahrain earnings going forward. The authors maintain positive views on UAE and Qatar due to a turnaround story in the former (Real Estate) and healthy growth in the latter

Market Liquidity: Value traded has picked up somewhat in 2011; 1H11 value traded came in at USD 194 bn, a 10% YoY growth. This was led by Saudi Arabia, where value traded in the first half of the year grew 28% YoY to USD 155 bn. Qatar was the only other GCC country to show a YoY growth in liquidity, at 33%. Kuwait registered a 47% YoY decline in 1H11 value traded to USD 13.5 bn. Given the positive YoY growth in liquidity so far this year, the report has a Positive view on the same for Saudi Arabia and Qatar while maintaining a Negative view on other markets.

(For rest of the parameters and a detailed explanation of the six forces framework refer to the report online at www.markaz.com/research

Kuwait Financial Centre 'Markaz', with total assets under management of over KD 960 million as of March 31st, 2011, was established in 1974 has become one of the leading asset management and investment banking institutions in the Arabian Gulf Region. Markaz was listed on the Kuwait Stock Exchange (KSE) in 1997